5 Euro (Piet Mondriaan) – Netherlands

Non-circulating coins

Commemoration: 150th Anniversary of the birth of Piet Mondriaan

Netherlands

Context

Material

Diameter: 33 mm

Weight: 15.5 g

Silver weight: 14.34 g

Shape: Round

Composition: 92.5% Silver

Standard: Silver half ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard431

Numista: #345199

Value

Exchange value: 5 EUR = $5.91

Bullion value: $39.74

Inflation-adjusted value: 5.85 EUR

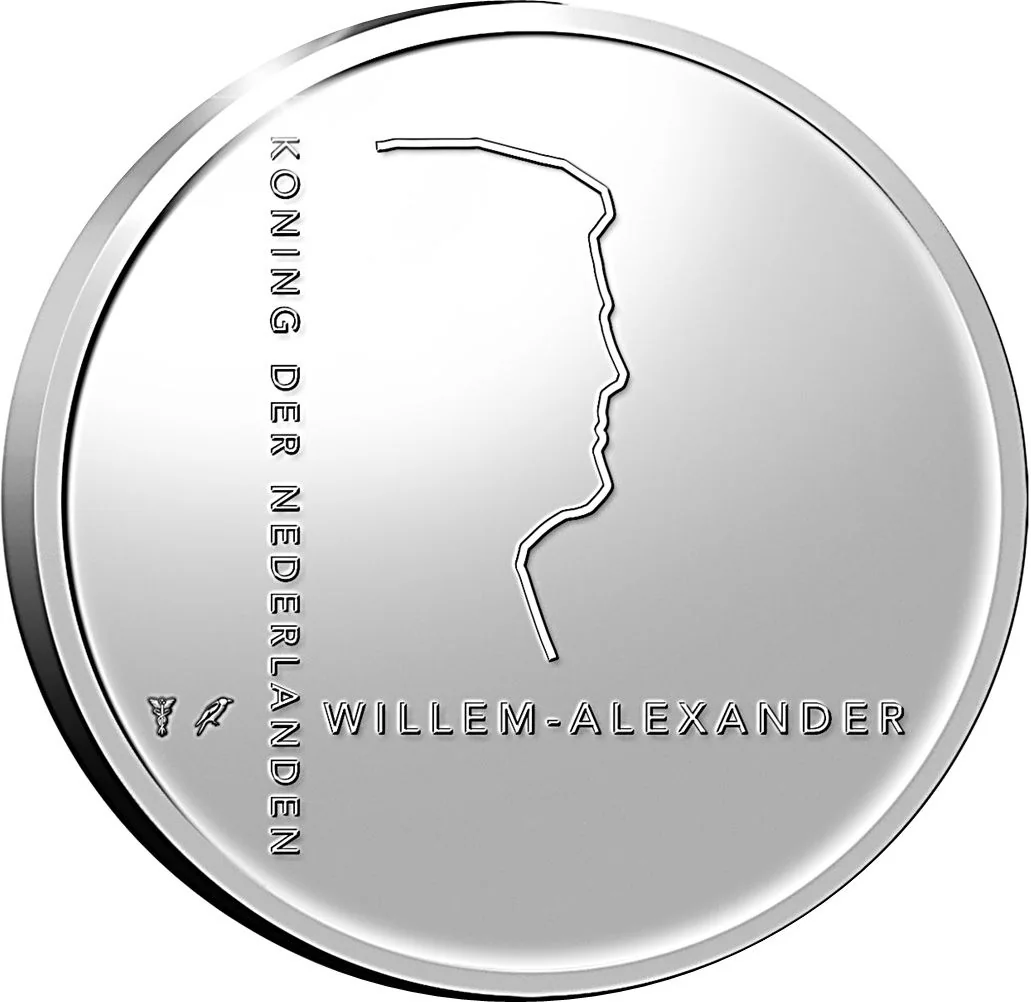

Obverse

Description:

A stylized depiction of King Willem-Alexander of the Netherlands.

Inscription:

KONING DER NEDERLANDEN

WILLEM-ALEXANDER

WILLEM-ALEXANDER

Translation:

King of the Netherlands

Willem-Alexander

Willem-Alexander

Script: Latin

Language: Dutch

Designer: Marjolein Rothman

Reverse

Edge

Smooth with inscriptions in hollow.

Legend:

GOD * ZIJ * MET * ONS

Translation:

God be with us

Language: Dutch

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2022 | — | 4,000 | Proof |

Historical background

In 2022, the Netherlands, as a founding member of the Eurozone, did not have an independent national currency policy, as its official currency was the euro. Therefore, the country's monetary situation was directly governed by the decisions of the European Central Bank (ECB). The year was dominated by the ECB's shifting policy in response to record-high inflation across the Eurozone, which peaked at over 10% in the Netherlands—significantly above the euro area average. This surge was driven by soaring energy prices due to the war in Ukraine, persistent supply chain disruptions, and strong post-pandemic consumer demand, creating a significant cost-of-living crisis for Dutch households and businesses.

The Dutch response was largely fiscal rather than monetary. The government implemented extensive national measures to shield consumers and companies from the energy price shock, including price caps on gas and electricity, energy bill allowances, and cuts to fuel taxes. These interventions, while crucial for social stability, also complicated the ECB's inflation-fighting efforts by maintaining aggregate demand. Furthermore, the Netherlands continued to advocate within the EU for a more hawkish ECB stance, reflecting its traditional concern for price stability and fiscal prudence.

Despite the inflationary pressures, the euro itself experienced significant volatility in 2022, depreciating sharply against the US dollar due to energy security fears and the relative monetary tightening of the Federal Reserve. This depreciation further imported inflation into the Dutch economy. By year's end, the ECB had initiated a historic series of interest rate hikes, marking a definitive end to the era of negative rates. Consequently, the Dutch financial landscape entered 2023 with tightening credit conditions, a cooling housing market, and an economic outlook focused on managing recession risks while bringing inflation under control.

The Dutch response was largely fiscal rather than monetary. The government implemented extensive national measures to shield consumers and companies from the energy price shock, including price caps on gas and electricity, energy bill allowances, and cuts to fuel taxes. These interventions, while crucial for social stability, also complicated the ECB's inflation-fighting efforts by maintaining aggregate demand. Furthermore, the Netherlands continued to advocate within the EU for a more hawkish ECB stance, reflecting its traditional concern for price stability and fiscal prudence.

Despite the inflationary pressures, the euro itself experienced significant volatility in 2022, depreciating sharply against the US dollar due to energy security fears and the relative monetary tightening of the Federal Reserve. This depreciation further imported inflation into the Dutch economy. By year's end, the ECB had initiated a historic series of interest rate hikes, marking a definitive end to the era of negative rates. Consequently, the Dutch financial landscape entered 2023 with tightening credit conditions, a cooling housing market, and an economic outlook focused on managing recession risks while bringing inflation under control.

💎 Extremely Rare