500 forint – Hungary

Add to wishlist

Non-circulating coins

Commemoration: Telstar 1 Satelite

Hungary

Context

Material

Diameter: 38.61 mm

Weight: 31.46 g

Silver Weight:: 29.10 g

Thickness: 3 mm

Shape: Round

Composition: 92.5% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #34384

Value

Exchange value: 500 HUF

Bullion value: $72.16

Inflation-adjusted value: 7606.32 HUF

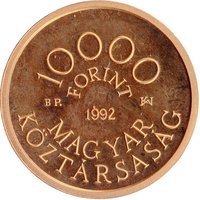

Obverse

Description:

Coat of arms left, text right and above.

Inscription:

MAGYAR KÖZTÁRSASÁG

500

FORINT

1992

BP.

BOGNÁR

500

FORINT

1992

BP.

BOGNÁR

Translation:

HUNGARIAN REPUBLIC

500

FORINT

1992

BP.

BOGNÁR

500

FORINT

1992

BP.

BOGNÁR

Script: Latin

Language: Hungarian

Engraver: György Bognár

Reverse

Description:

Telstar 1 orbiting Earth.

Inscription:

TELSTAR 1 1962

Script: Latin

Engraver: György Bognár

Edge

Reeded

Categories

| Space |

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP. |

Historical background

In 1992, Hungary was navigating a complex and fragile monetary transition following the political changes of 1989-90. The country operated with a non-convertible forint, its value strictly managed by the National Bank of Hungary within a "crawling peg" system. This mechanism involved small, pre-announced devaluations (roughly 1-2% per month) against a basket of hard currencies, primarily the US Dollar and German Mark. This policy aimed to balance competing goals: maintaining export competitiveness through gradual devaluation while cautiously taming an inherited inflation rate that still hovered around 20-25% annually.

The currency situation was fundamentally constrained by the lack of full convertibility. While some progress had been made—allowing for limited convertibility for current account transactions—strict capital controls remained in place. This created a dual exchange rate system: an official rate for legitimate trade and a much weaker black-market rate for those seeking to move capital abroad. The government and central bank were under significant pressure from international institutions, like the IMF, to accelerate reforms toward full convertibility, but fears of capital flight and currency collapse made authorities exceedingly cautious.

Overall, the 1992 forint was a currency in a state of managed transition, reflecting the broader challenges of shifting from a planned to a market economy. The crawling peg provided stability but was a temporary tool in the face of persistent inflation and pent-up demand for foreign currency. The situation underscored the tension between the need for macroeconomic stabilization and the political and social pressures of a transforming society, setting the stage for more decisive reforms later in the decade.

The currency situation was fundamentally constrained by the lack of full convertibility. While some progress had been made—allowing for limited convertibility for current account transactions—strict capital controls remained in place. This created a dual exchange rate system: an official rate for legitimate trade and a much weaker black-market rate for those seeking to move capital abroad. The government and central bank were under significant pressure from international institutions, like the IMF, to accelerate reforms toward full convertibility, but fears of capital flight and currency collapse made authorities exceedingly cautious.

Overall, the 1992 forint was a currency in a state of managed transition, reflecting the broader challenges of shifting from a planned to a market economy. The crawling peg provided stability but was a temporary tool in the face of persistent inflation and pent-up demand for foreign currency. The situation underscored the tension between the need for macroeconomic stabilization and the political and social pressures of a transforming society, setting the stage for more decisive reforms later in the decade.

⭐ Rare