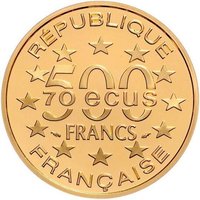

500 Francs – France

France

Context

Year: 1993

Issuer: France

Period:

(since 1958)

Currency:

(1960—2001)

Subdivision: 500 Francs = 70 ECU

Demonetized: Yes

Total mintage: 3,000

Material

References

KM: #Click to copy to clipboard1033

Numista: #335876

Value

Exchange value: 500 FRF

Bullion value: $2612.94

Inflation-adjusted value: 864.16 FRF

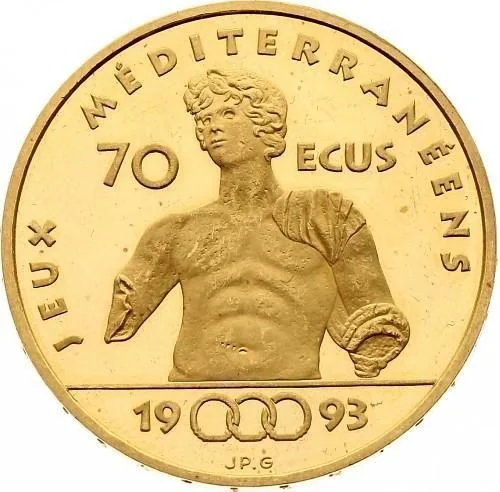

Obverse

Description:

Portrait of Marianne encircled by text.

Inscription:

RÉPUBLIQUE FRANÇAISE

500 F

JP.GENDIS

500 F

JP.GENDIS

Translation:

FRENCH REPUBLIC

500 F

JP.GENDIS

500 F

JP.GENDIS

Script: Latin

Language: French

Engraver: Jean-Pierre Gendis

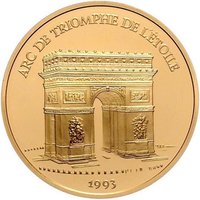

Reverse

Edge

Plain

Legend:

LIBERTE*EGALITE*FRATERNITE**

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1993 | — | 3,000 | Proof |

Historical background

In 1993, France's currency situation was defined by its pivotal role within the European Exchange Rate Mechanism (ERM), the system designed to stabilize currencies ahead of the planned single currency. The French franc was a cornerstone of this mechanism, famously maintaining a strong and stable parity against the Deutsche Mark within narrow fluctuation bands. This policy, known as the franc fort (strong franc), was a strategic commitment by French authorities to align closely with Germany's low-inflation Bundesbank, aiming to import monetary credibility and lay the groundwork for European Monetary Union.

However, this stability was maintained under severe pressure. The year followed the 1992 ERM crisis, which had forced the devaluation of several currencies, including the British pound's exit from the mechanism. Speculative attacks now focused on the franc in 1993, as markets doubted France's ability to sustain high German interest rates amidst a deep domestic recession and rising unemployment. The Bundesbank's reluctance to cut rates to aid its partners created immense tension, testing the Franco-German axis at the heart of the European project.

The climax came in July-August 1993. After a massive coordinated intervention failed to deter speculators, European finance ministers were forced into an emergency weekend meeting. Their solution, announced on August 2, was a radical temporary fix: the fluctuation bands for most ERM currencies were dramatically widened to ±15%, effectively allowing the franc to devalue modestly while remaining within the system. This compromise saved the ERM from collapse and preserved the path to the single currency, but it underscored the extreme sacrifices required by the franc fort policy and highlighted the difficult transition toward ceding national monetary sovereignty.

However, this stability was maintained under severe pressure. The year followed the 1992 ERM crisis, which had forced the devaluation of several currencies, including the British pound's exit from the mechanism. Speculative attacks now focused on the franc in 1993, as markets doubted France's ability to sustain high German interest rates amidst a deep domestic recession and rising unemployment. The Bundesbank's reluctance to cut rates to aid its partners created immense tension, testing the Franco-German axis at the heart of the European project.

The climax came in July-August 1993. After a massive coordinated intervention failed to deter speculators, European finance ministers were forced into an emergency weekend meeting. Their solution, announced on August 2, was a radical temporary fix: the fluctuation bands for most ERM currencies were dramatically widened to ±15%, effectively allowing the franc to devalue modestly while remaining within the system. This compromise saved the ERM from collapse and preserved the path to the single currency, but it underscored the extreme sacrifices required by the franc fort policy and highlighted the difficult transition toward ceding national monetary sovereignty.

✨ Legendary