5 Emalangeni (Central Bank) – Kingdom of Swaziland

Circulating commemorative coins

Commemoration: Central Bank's 25th Anniversary

Eswatini

Context

Year: 1999

Country: Eswatini

Issuer: Kingdom of Swaziland

Ruler: Mswati III

Currency:

(1974—2018)

Demonetization: 1 February 2016

Material

References

KM: #Click to copy to clipboard53

Numista: #3343

Value

Exchange value: 5 SZL

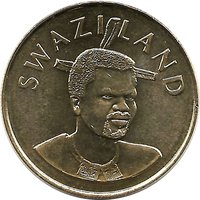

Obverse

Reverse

Description:

Bank seal: circle, hut, trees, cow.

Inscription:

25th ANNIVERSARY CENTRAL BANK OF SWAZILAND

EMNTSHOLI

1974 - 1999

5 EMALANGENI

EMNTSHOLI

1974 - 1999

5 EMALANGENI

Script: Latin

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1999 | — | — |

Historical background

In 1999, the Kingdom of Swaziland (renamed Eswatini in 2018) operated within a unique and tightly managed currency regime as a member of the Common Monetary Area (CMA) with South Africa, Lesotho, and Namibia. The country's currency, the lilangeni (plural: emalangeni), was pegged at par to the South African rand, which was also legal tender within the kingdom. This arrangement effectively ceded Swaziland's monetary policy to the South African Reserve Bank, ensuring stability and facilitating trade but limiting domestic policy tools to respond to local economic conditions.

The year 1999 fell within a period of relative macroeconomic stability for Swaziland, though underlying challenges persisted. The fixed peg provided low inflation and exchange rate certainty, which benefited the economy's strong trade and financial links with South Africa. However, the kingdom's fiscal position was a growing concern, with government expenditures rising steadily, often financed through drawdowns from foreign reserves. This practice raised questions about the long-term sustainability of the peg, as the country's ability to maintain the required reserve backing was crucial for CMA compliance.

Furthermore, the economy remained heavily dependent on sugar exports and revenue from the Southern African Customs Union (SACU), making it vulnerable to external shocks. While the currency situation itself was stable in 1999, the structural weaknesses in the Swazi economy—including limited diversification, high unemployment, and fiscal pressures—posed indirect risks to the monetary arrangement. The government's challenge was to manage its finances prudently to maintain the credibility of the peg while navigating the social and economic demands of a young and growing population.

The year 1999 fell within a period of relative macroeconomic stability for Swaziland, though underlying challenges persisted. The fixed peg provided low inflation and exchange rate certainty, which benefited the economy's strong trade and financial links with South Africa. However, the kingdom's fiscal position was a growing concern, with government expenditures rising steadily, often financed through drawdowns from foreign reserves. This practice raised questions about the long-term sustainability of the peg, as the country's ability to maintain the required reserve backing was crucial for CMA compliance.

Furthermore, the economy remained heavily dependent on sugar exports and revenue from the Southern African Customs Union (SACU), making it vulnerable to external shocks. While the currency situation itself was stable in 1999, the structural weaknesses in the Swazi economy—including limited diversification, high unemployment, and fiscal pressures—posed indirect risks to the monetary arrangement. The government's challenge was to manage its finances prudently to maintain the credibility of the peg while navigating the social and economic demands of a young and growing population.

🌱 Fairly Common