20 Francs – Belgium

Belgium

Context

Years: 1867–1870

Issuer: Belgium

Ruler: Leopold II

Currency:

(1832—2001)

Demonetization: 20 April 1957

Total mintage: 7,148,733

Material

References

KM: #Click to copy to clipboard32

Numista: #13801

Value

Exchange value: 20 BEF

Bullion value: $969.51

Obverse

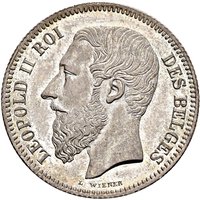

Description:

King Leopold II facing right with French lettering. Date and designer below.

Inscription:

LEOPOLD II ROI DES BELGES

L W

1868

L W

1868

Translation:

Leopold II King of the Belgians

L W

1868

L W

1868

Script: Latin

Language: French

Engraver: Léopold Wiener

Reverse

Description:

Belgian crowned coat of arms with French motto above, value below.

Inscription:

L'UNION FAIT LA FORCE

20 FR.

20 FR.

Translation:

Union Makes Strength

20 Francs

20 Francs

Script: Latin

Language: French

Engraver: Léopold Wiener

Edge

Plain with raised lettering

Legend:

DIEU * PROTEGE * LA * BELGIQUE *****

Translation:

GOD * PROTECT * BELGIQUE

Language: French

Categories

| Symbol> Crown |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1867 | — | 1,341,307 | ||

| 1868 | — | 1,381,749 | ||

| 1869 | — | 1,234,474 | ||

| 1870 | — | 3,191,203 |

Historical background

In 1867, Belgium operated under a complex and transitional monetary system, a legacy of its recent independence and the broader European context. The country was part of the Latin Monetary Union (LMU), established in 1865, which Belgium had helped found alongside France, Italy, and Switzerland. This agreement aimed to standardize coinage by fixing the silver content and gold-to-silver ratio, allowing the coins of member nations to circulate freely across borders. Belgium's national currency, the Belgian franc, was thus pegged to this bimetallic standard, with its value defined as equal to the French franc.

However, the system was under significant strain by 1867. The LMU's bimetallism was being destabilized by the global fluctuation in the relative market values of gold and silver. An overvaluation of silver within the Union led to an influx of silver coins, while gold coins were often hoarded or exported. This created practical difficulties for commerce and government finance, as the intended parity between the metals was artificial and difficult to maintain. Belgium, as a small, trade-dependent nation, felt these pressures acutely, with concerns about the loss of monetary sovereignty and the practical costs of maintaining a circulating medium.

Consequently, 1867 was a year of debate and looming decision. While the LMU framework provided stability for international trade, its inherent flaws were becoming apparent. Belgian policymakers and financiers were engaged in discussions about the future, weighing the benefits of the Union against the need for a more stable, perhaps gold-based, system. The situation was a microcosm of a global monetary debate, positioning Belgium at a crossroads between the old bimetallic order and the emerging gold standard that would come to dominate the subsequent decades.

However, the system was under significant strain by 1867. The LMU's bimetallism was being destabilized by the global fluctuation in the relative market values of gold and silver. An overvaluation of silver within the Union led to an influx of silver coins, while gold coins were often hoarded or exported. This created practical difficulties for commerce and government finance, as the intended parity between the metals was artificial and difficult to maintain. Belgium, as a small, trade-dependent nation, felt these pressures acutely, with concerns about the loss of monetary sovereignty and the practical costs of maintaining a circulating medium.

Consequently, 1867 was a year of debate and looming decision. While the LMU framework provided stability for international trade, its inherent flaws were becoming apparent. Belgian policymakers and financiers were engaged in discussions about the future, weighing the benefits of the Union against the need for a more stable, perhaps gold-based, system. The situation was a microcosm of a global monetary debate, positioning Belgium at a crossroads between the old bimetallic order and the emerging gold standard that would come to dominate the subsequent decades.

🌟 Uncommon