100 Bahts – Thailand

Circulating commemorative coins

Commemoration: World Bank - Internat. Monetary Fund

Thailand

Context

Year: 1991

Thai Year: 2534

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Total mintage: 560,000

Material

Diameter: 38 mm

Weight: 25 g

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

Y: #Click to copy to clipboard242

Numista: #13795

Value

Exchange value: 100 THB = $3.22

Obverse

Description:

Busts of King Bhumibol Adulyadej and Queen Sirikit in royal attire, wearing the collars of the Order of the Royal House of Chakri. The Queen also wears the King's royal cypher medal. Their royal cyphers appear on the sides.

Inscription:

พ.ศ.๒๕๓๔ . ประเทศไทย . ๑๐๐ บาท

Translation:

B.E. 2534 . Thailand . 100 Baht

Language: Thai

Reverse

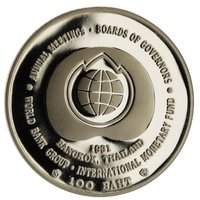

Description:

Meeting logo.

Inscription:

. ANNUAL MEETINGS . BOARDS OF GOVERNORS .

1991

BANGKOK THAILAND

WORLD BANK GROUP . INTERNATIONAL MONETARY FUND

100 BAHT

1991

BANGKOK THAILAND

WORLD BANK GROUP . INTERNATIONAL MONETARY FUND

100 BAHT

Edge

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1991 | — | 500,000 | ||

| 1991 | — | 60,000 | Proof |

Historical background

In 1991, Thailand's currency, the baht, operated under a tightly managed exchange rate system, pegged to a basket of currencies heavily weighted toward the U.S. dollar. This policy, maintained by the Bank of Thailand (BOT), provided stability for trade and investment, which was crucial for an export-oriented economy experiencing rapid growth. The peg was widely seen as a cornerstone of Thailand's economic success, fostering confidence among foreign investors and contributing to the country's reputation as an emerging "Asian Tiger." Inflation was relatively low, and the economy was booming, with GDP growth exceeding 8% that year.

However, underlying pressures were beginning to emerge. Thailand's large current account deficit, fueled by strong import growth and a high level of foreign-denominated debt in the private sector, created a vulnerability. The baht's peg, while stable, was perceived by some economists as potentially overvalued, making Thai exports less competitive just as regional rivals were devaluing their currencies. Furthermore, the country's financial liberalization in the late 1980s had opened the capital account, allowing for large inflows of "hot money" seeking high returns, which increased the economy's exposure to sudden shifts in investor sentiment.

The political context added another layer of complexity. The year 1991 began under the unelected government of Prime Minister Chatichai Choonhavan, which was overthrown by a military coup in February. The subsequent National Peace Keeping Council, led by General Suchinda Kraprayoon, initially pledged pro-market policies but introduced political uncertainty. Despite this turbulence, the currency regime itself was not yet in crisis; the severe pressures that would culminate in the 1997 Asian Financial Crisis were still gathering force. Thus, 1991 represents a point of apparent stability, but one where the foundations for future turmoil were being laid.

However, underlying pressures were beginning to emerge. Thailand's large current account deficit, fueled by strong import growth and a high level of foreign-denominated debt in the private sector, created a vulnerability. The baht's peg, while stable, was perceived by some economists as potentially overvalued, making Thai exports less competitive just as regional rivals were devaluing their currencies. Furthermore, the country's financial liberalization in the late 1980s had opened the capital account, allowing for large inflows of "hot money" seeking high returns, which increased the economy's exposure to sudden shifts in investor sentiment.

The political context added another layer of complexity. The year 1991 began under the unelected government of Prime Minister Chatichai Choonhavan, which was overthrown by a military coup in February. The subsequent National Peace Keeping Council, led by General Suchinda Kraprayoon, initially pledged pro-market policies but introduced political uncertainty. Despite this turbulence, the currency regime itself was not yet in crisis; the severe pressures that would culminate in the 1997 Asian Financial Crisis were still gathering force. Thus, 1991 represents a point of apparent stability, but one where the foundations for future turmoil were being laid.

⭐ Somewhat Rare