1 lats – Latvia

Add to wishlist

Non-circulating coins

Commemoration: Coin of Water

Latvia

Context

Material

Weight: 26 g

Silver Weight:: 24.05 g

Shape: Square with angled corners

Composition: 92.5% Silver

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #30564

Value

Exchange value: 1 LVL

Bullion value: $58.99

Inflation-adjusted value: 1.61 LVL

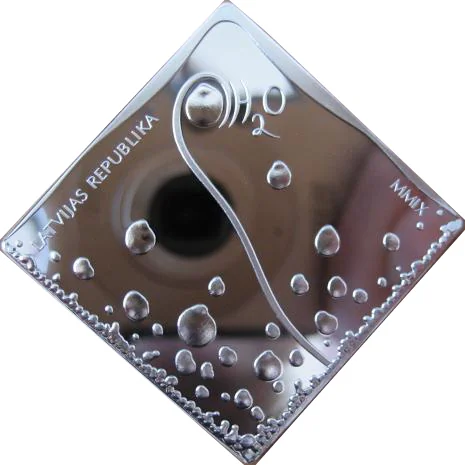

Obverse

Description:

A water drop path begins at the central H2O inscription, set against a background of smaller drops. "LATVIJAS REPUBLIKA" arcs along the lower left edge, and "MMIX" (2009) arcs along the lower right.

Inscription:

LATVIJAS REPUBLIKA

MMIX

MMIX

Translation:

REPUBLIC OF LATVIA

2009

2009

Engraver: Jānis Strupulis

Designer: Ilmārs Blumbergs

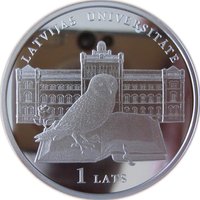

Reverse

Description:

A water crystal is centered on the coin, with "1 LATS" inscribed along the lower right side.

Inscription:

1 LATS

Engraver: Jānis Strupulis

Designer: Ilmārs Blumbergs

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mint of Finland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2009 | — | 7,000 | Proof |

Historical background

In 2009, Latvia faced a severe currency crisis as a direct consequence of the global financial meltdown, which exposed the profound vulnerabilities of its overheated economy. During the preceding boom years, fueled by easy credit primarily from Scandinavian banks, Latvia had accumulated massive external imbalances and one of the highest current account deficits in Europe. When capital flows abruptly reversed in late 2008, the economy contracted violently, the banking system teetered on the brink, and the government was forced to seek an international bailout to avoid bankruptcy.

The core of the crisis centered on maintaining the Latvian lat’s fixed peg to the euro, a policy cornerstone since the currency's reintroduction in 1993. Devaluation was fiercely debated, as it could have provided immediate relief for exporters but would have crippled households and businesses with euro-denominated debts and risked triggering a regional banking crisis in Sweden and the Baltics. Ultimately, the Latvian government, under pressure from the European Commission and the International Monetary Fund (IMF), chose an "internal devaluation" strategy. This involved accepting a €7.5 billion rescue package in exchange for implementing brutal austerity measures—deep cuts to public sector wages and pensions, and radical reductions in government spending—to restore competitiveness and defend the peg.

The social and economic cost was staggering. Latvia experienced the deepest recession in the European Union in 2009, with GDP plummeting by over 17%. Unemployment soared, and significant emigration ensued. However, the strategy succeeded in its primary goal: the lat's peg to the euro held firm. This painful period of internal devaluation paved the way for Latvia's eventual adoption of the euro in 2014, which was seen as the final consolidation of the currency stability that had been preserved at such a high cost during the crisis.

The core of the crisis centered on maintaining the Latvian lat’s fixed peg to the euro, a policy cornerstone since the currency's reintroduction in 1993. Devaluation was fiercely debated, as it could have provided immediate relief for exporters but would have crippled households and businesses with euro-denominated debts and risked triggering a regional banking crisis in Sweden and the Baltics. Ultimately, the Latvian government, under pressure from the European Commission and the International Monetary Fund (IMF), chose an "internal devaluation" strategy. This involved accepting a €7.5 billion rescue package in exchange for implementing brutal austerity measures—deep cuts to public sector wages and pensions, and radical reductions in government spending—to restore competitiveness and defend the peg.

The social and economic cost was staggering. Latvia experienced the deepest recession in the European Union in 2009, with GDP plummeting by over 17%. Unemployment soared, and significant emigration ensued. However, the strategy succeeded in its primary goal: the lat's peg to the euro held firm. This painful period of internal devaluation paved the way for Latvia's eventual adoption of the euro in 2014, which was seen as the final consolidation of the currency stability that had been preserved at such a high cost during the crisis.

💎 Very Rare