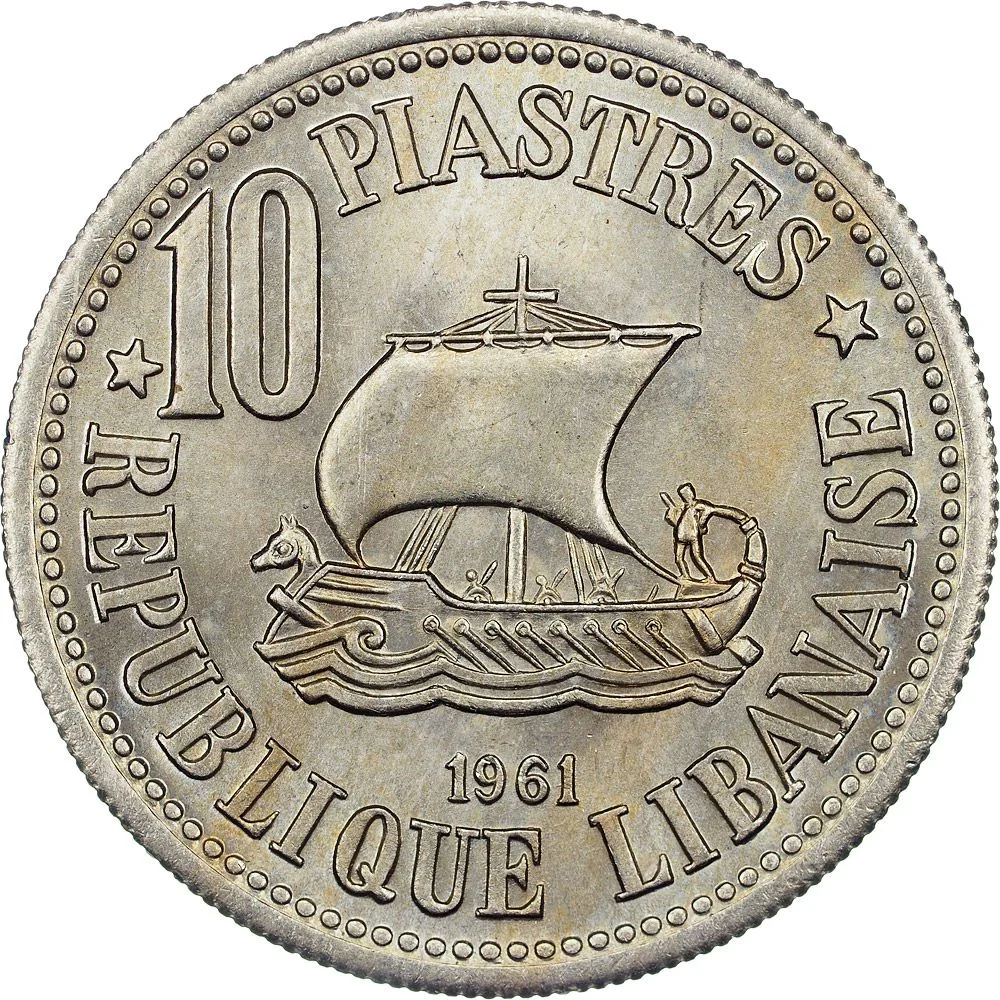

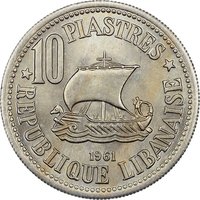

10 piastres – Lebanon

Add to wishlist

Lebanon

Context

Year: 1961

Issuer: Lebanon

Period:

(since 1943)

Currency:

(since 1939)

Demonetized: Yes

Total mintage: 7,000,000

Material

References

KM: #

Numista: #3008

Value

Exchange value: 0.10 LBP

Obverse

Reverse

Edge

Milled

Categories

| Plant> Tree |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1961 | — | 7,000,000 | ||

| 1961 | — | — | Proof |

Historical background

In 1961, Lebanon's currency situation was one of notable stability and confidence, underpinned by the strength of the Lebanese pound (LBP). The country was in the midst of its "Golden Age," a period of significant economic growth and prosperity driven by its role as a regional banking, trade, and tourism hub. The Lebanese pound was freely convertible and pegged to the French franc, a legacy of the French Mandate, at a rate of approximately 3.5 LBP to 1 US dollar. This fixed and credible peg, maintained by the Banque du Liban (the central bank, established in 1964), facilitated international commerce and attracted substantial capital inflows, reinforcing Beirut's status as the "Switzerland of the Middle East."

This monetary stability was not accidental but was built upon a foundation of conservative fiscal policy and a laissez-faire economic model. The government generally maintained balanced budgets and avoided excessive foreign borrowing, while the banking sector thrived under strict secrecy laws. The country's substantial gold reserves, coupled with a persistent current account surplus from service exports and remittances, provided a solid buffer to support the currency's peg. Consequently, the Lebanese pound was considered a strong and reliable store of value, both domestically and regionally.

However, this picture of robustness contained the early seeds of future vulnerabilities. The economy's structure was increasingly skewed towards services and finance, with a growing reliance on imported goods, including basic necessities. While not a crisis in 1961, this import dependency made the country sensitive to trade imbalances. Furthermore, the political landscape, though stable on the surface, was delicately balanced on sectarian lines. The economic model's success depended entirely on continued political consensus, fiscal discipline, and uninterrupted capital inflows—conditions that would dramatically shift in the coming decades, leading to the profound currency crisis that began in 2019.

This monetary stability was not accidental but was built upon a foundation of conservative fiscal policy and a laissez-faire economic model. The government generally maintained balanced budgets and avoided excessive foreign borrowing, while the banking sector thrived under strict secrecy laws. The country's substantial gold reserves, coupled with a persistent current account surplus from service exports and remittances, provided a solid buffer to support the currency's peg. Consequently, the Lebanese pound was considered a strong and reliable store of value, both domestically and regionally.

However, this picture of robustness contained the early seeds of future vulnerabilities. The economy's structure was increasingly skewed towards services and finance, with a growing reliance on imported goods, including basic necessities. While not a crisis in 1961, this import dependency made the country sensitive to trade imbalances. Furthermore, the political landscape, though stable on the surface, was delicately balanced on sectarian lines. The economic model's success depended entirely on continued political consensus, fiscal discipline, and uninterrupted capital inflows—conditions that would dramatically shift in the coming decades, leading to the profound currency crisis that began in 2019.

🌱 Very Common