10 Francs – France

France

Context

Years: 1991–2001

Issuer: France

Period:

(since 1958)

Currency:

(1960—2001)

Demonetization: 17 February 2005

Total mintage: 104,141

Material

References

KM: #Click to copy to clipboard964.2

Numista: #284996

Value

Exchange value: 10 FRF

Inflation-adjusted value: 18.26 FRF

Obverse

Description:

The winged Genius of Liberty, holding a torch, is flanked by the letters "R" and "F" for République française. The periphery features striated geometric motifs, with the engraving workshop's name (AGMM) below the "R." This design replicates Auguste Dumont's gilded sculpture atop the July Column in Paris, which commemorates the July Revolution of 1830.

Inscription:

R F

Translation:

Rex Francorum

Script: Latin

Language: Latin

Engraver: Jean-Luc Maréchal

Reverse

Description:

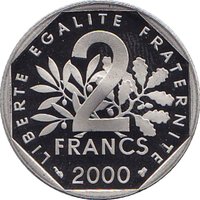

The coin features "LIBERTÉ ÉGALITÉ FRATERNITÉ" encircling a central "10 F", the year, and mint marks, against a striated triangular background.

Inscription:

LIBERTÉ EGALITÉ

10 F

1994

FRATERNITÉ

10 F

1994

FRATERNITÉ

Translation:

LIBERTY EQUALITY

10 F

1994

FRATERNITY

10 F

1994

FRATERNITY

Script: Latin

Language: French

Engraver: Jean-Luc Maréchal

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1991 | — | 6,232 | ||

| 1992 | — | 4,938 | ||

| 1993 | — | 5,309 | ||

| 1994 | — | 3,707 | ||

| 1995 | — | 4,796 | ||

| 1996 | — | 5,319 | ||

| 1997 | — | 6,436 | ||

| 1998 | — | 7,404 | ||

| 1999 | — | 10,000 | ||

| 2000 | — | 15,000 | ||

| 2001 | — | 35,000 |

Historical background

In 1991, France's currency situation was defined by its pivotal role within the European Monetary System (EMS) and the ongoing march toward Economic and Monetary Union (EMU). The French franc was a central pillar of the Exchange Rate Mechanism (ERM), a system designed to limit currency fluctuations between member states. France, alongside Germany, was a key architect and staunch defender of this mechanism, viewing exchange rate stability as a cornerstone for deeper European integration and a necessary precursor to a single currency. This commitment was part of a broader French political consensus to anchor the nation firmly within a integrated Europe, often using monetary policy as a tool to reinforce this strategic alignment.

Domestically, this commitment came at a significant cost. To maintain the franc's strong parity with the Deutsche Mark—the anchor currency of the ERM—the Banque de France was required to follow a high-interest rate policy set by Germany's Bundesbank. This policy was particularly challenging as Germany raised rates to combat inflation following its reunification, a move that did not align with France's weaker economic cycle. Consequently, France endured a period of "franc fort" (strong franc) policy, which prioritized currency stability over domestic growth, contributing to subdued economic activity and higher unemployment.

The tensions of this period set the stage for the severe crises that would follow in 1992 and 1993, when speculative attacks tested the ERM's limits. However, in 1991, the system was still holding, and France was actively participating in the final negotiations of the Maastricht Treaty. The year was thus one of determined, albeit strained, preparation, with France working to meet the strict convergence criteria—on inflation, interest rates, budget deficits, and debt—that would qualify it for the planned single European currency, the future euro.

Domestically, this commitment came at a significant cost. To maintain the franc's strong parity with the Deutsche Mark—the anchor currency of the ERM—the Banque de France was required to follow a high-interest rate policy set by Germany's Bundesbank. This policy was particularly challenging as Germany raised rates to combat inflation following its reunification, a move that did not align with France's weaker economic cycle. Consequently, France endured a period of "franc fort" (strong franc) policy, which prioritized currency stability over domestic growth, contributing to subdued economic activity and higher unemployment.

The tensions of this period set the stage for the severe crises that would follow in 1992 and 1993, when speculative attacks tested the ERM's limits. However, in 1991, the system was still holding, and France was actively participating in the final negotiations of the Maastricht Treaty. The year was thus one of determined, albeit strained, preparation, with France working to meet the strict convergence criteria—on inflation, interest rates, budget deficits, and debt—that would qualify it for the planned single European currency, the future euro.

🌱 Fairly Common