¼ dollar – United States

Add to wishlist

Non-circulating coins

Commemoration: Tallgrass Prairie National Preserve Series: America the Beautiful Quarters® Program

United States

Context

Year: 2020

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Subdivision: ¼ dollar = 25 Cents

Material

Diameter: 76.2 mm

Weight: 155.52 g

Silver Weight:: 155.36 g

Thickness: 4.19 mm

Shape: Round

Composition: 99.9% Silver

Standard: Silver 5 ounces

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #266326

Value

Exchange value: ¼ USD = $0.25

Bullion value: $378.11

Inflation-adjusted value: 0.31 USD

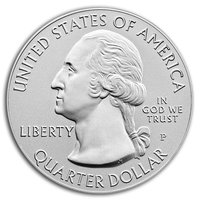

Obverse

Description:

Left-profile portrait of George Washington, U.S. President (1789-1797).

Inscription:

UNITED STATES OF AMERICA

IN

GOD WE

TRUST

LIBERTY P

JF WC

QUARTER DOLLAR

IN

GOD WE

TRUST

LIBERTY P

JF WC

QUARTER DOLLAR

Script: Latin

Engravers: John Flanagan, William Cousins

Reverse

Description:

A Regal Fritillary butterfly ascends against a backdrop of iconic Tallgrass Prairie grasses, Big Bluestem and Indian grass.

Inscription:

TALLGRASS PRAIRIE

KANSAS

2020

E PLURIBUS UNUM

KANSAS

2020

E PLURIBUS UNUM

Script: Latin

Engravers: Renata Gordon, Emily S. Damstra

Edge

Reeded

Categories

| Animal> Insect |

| Person> Military leader |

| Person> Politician |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2020 | — | — |

Historical background

The United States entered 2020 with a relatively stable currency environment, but the COVID-19 pandemic triggered an unprecedented economic and monetary policy response that profoundly impacted the U.S. dollar. As lockdowns began in March, a global dash for cash caused a dramatic, short-lived surge in the dollar's value against other major currencies, reflecting its enduring role as the world's premier safe-haven asset. This "dollar shortage" threatened global financial stability, prompting the Federal Reserve to activate emergency currency swap lines with other central banks to provide liquidity and calm international markets.

Domestically, the Federal Reserve slashed interest rates to near zero and launched a massive quantitative easing program, purchasing trillions of dollars in Treasury and mortgage-backed securities. Concurrently, Congress passed historic fiscal stimulus packages, notably the $2.2 trillion CARES Act, injecting direct payments and expanded unemployment benefits into the economy. This combination of expansive monetary policy and aggressive fiscal spending was designed to prevent a deflationary spiral and support households and businesses, but it also significantly expanded the money supply and the national debt.

By the second half of 2020, the initial dollar strength had reversed into a sustained decline. As investor risk appetite returned and the Fed's commitment to low rates solidified, the dollar index fell to multi-year lows. This depreciation was viewed as a result of the ballooning U.S. deficit, ultra-low yields making dollar assets less attractive, and growing optimism about a global recovery that would benefit other currencies. Thus, the year encapsulated the dollar's dual nature: its initial spike demonstrated its critical global role in a crisis, while its subsequent weakening reflected the long-term inflationary and debt implications of the policy choices made to combat the pandemic's economic shock.

Domestically, the Federal Reserve slashed interest rates to near zero and launched a massive quantitative easing program, purchasing trillions of dollars in Treasury and mortgage-backed securities. Concurrently, Congress passed historic fiscal stimulus packages, notably the $2.2 trillion CARES Act, injecting direct payments and expanded unemployment benefits into the economy. This combination of expansive monetary policy and aggressive fiscal spending was designed to prevent a deflationary spiral and support households and businesses, but it also significantly expanded the money supply and the national debt.

By the second half of 2020, the initial dollar strength had reversed into a sustained decline. As investor risk appetite returned and the Fed's commitment to low rates solidified, the dollar index fell to multi-year lows. This depreciation was viewed as a result of the ballooning U.S. deficit, ultra-low yields making dollar assets less attractive, and growing optimism about a global recovery that would benefit other currencies. Thus, the year encapsulated the dollar's dual nature: its initial spike demonstrated its critical global role in a crisis, while its subsequent weakening reflected the long-term inflationary and debt implications of the policy choices made to combat the pandemic's economic shock.

💎 Extremely Rare