½ dinar – Jordan

Add to wishlist

Jordan

Context

Year: 1997

Islamic (Hijri) Year:: 1417

Issuer: Jordan

Ruler: Hussein bin Talal

Currency:

(since 1949)

Material

Diameter: 29 mm

Weight: 9.6 g

Thickness: 1.94 mm

Shape: Equilateral curve heptagon

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #2618

Value

Exchange value: ½ JOD

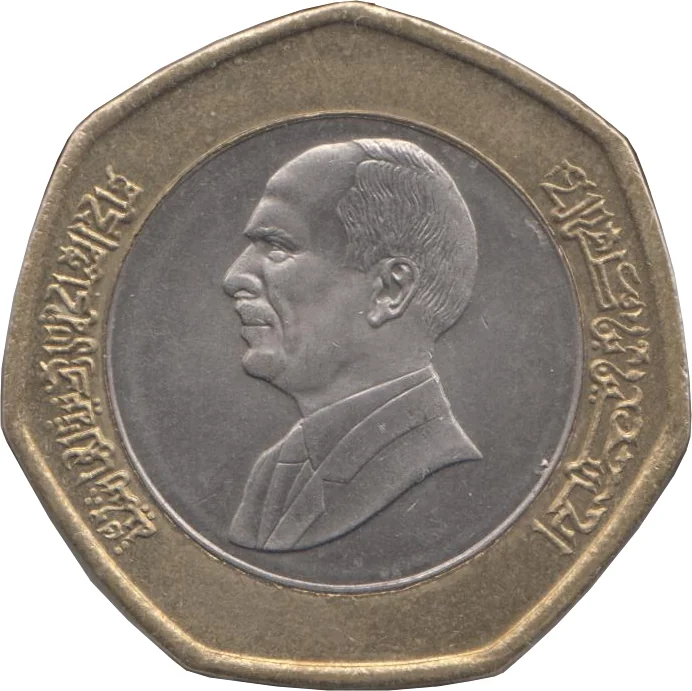

Obverse

Description:

King Hussein bust, left, encircled by legend.

Inscription:

الحسين بن طلال

ملك المملكة الأردنية الهاشمية

ملك المملكة الأردنية الهاشمية

Translation:

Hussein bin Talal

King of the Hashemite Kingdom of Jordan

King of the Hashemite Kingdom of Jordan

Language: Arabic

Reverse

Edge

Plain

Categories

| Person> Monarch |

| Mustache/Beard |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | — |

Historical background

In 1997, Jordan's currency, the dinar (JOD), was a notable pillar of stability in a region often marked by economic volatility. This stability was the direct result of a fixed exchange rate regime, pegged to the U.S. dollar since 1995 at a rate of approximately 0.709 JOD per dollar, with only a narrow band for fluctuation. This policy, managed by the Central Bank of Jordan (CBJ), was a cornerstone of the country's economic strategy, designed to control inflation, attract foreign investment, and provide a predictable environment for trade. The peg was broadly successful in achieving these goals, fostering confidence in the dinar both domestically and internationally.

However, this monetary stability existed against a backdrop of significant economic challenges. The economy was burdened by high public debt, persistent budget deficits, and sluggish growth. Structural adjustment programs agreed with the International Monetary Fund (IMF) throughout the early 1990s had imposed austerity measures, including reductions in subsidies, which placed pressure on living standards. Furthermore, Jordan's reliance on remittances, foreign aid (particularly following the 1994 peace treaty with Israel), and phosphate exports made its economy vulnerable to external shocks. The fixed exchange rate, while stabilizing prices, also limited the CBJ's ability to use monetary policy as a tool to stimulate the domestic economy.

Consequently, the currency situation in 1997 was one of surface-level calm masking underlying strains. The dinar's peg was firmly maintained and not under immediate threat, but the sustainability of this regime was dependent on continued access to foreign grants and concessional financing to support the country's foreign reserves. Policymakers were thus walking a tightrope, balancing the undeniable benefits of a strong, fixed currency against the mounting costs of maintaining it in the face of structural economic weaknesses and the social pressures stemming from ongoing economic reforms.

However, this monetary stability existed against a backdrop of significant economic challenges. The economy was burdened by high public debt, persistent budget deficits, and sluggish growth. Structural adjustment programs agreed with the International Monetary Fund (IMF) throughout the early 1990s had imposed austerity measures, including reductions in subsidies, which placed pressure on living standards. Furthermore, Jordan's reliance on remittances, foreign aid (particularly following the 1994 peace treaty with Israel), and phosphate exports made its economy vulnerable to external shocks. The fixed exchange rate, while stabilizing prices, also limited the CBJ's ability to use monetary policy as a tool to stimulate the domestic economy.

Consequently, the currency situation in 1997 was one of surface-level calm masking underlying strains. The dinar's peg was firmly maintained and not under immediate threat, but the sustainability of this regime was dependent on continued access to foreign grants and concessional financing to support the country's foreign reserves. Policymakers were thus walking a tightrope, balancing the undeniable benefits of a strong, fixed currency against the mounting costs of maintaining it in the face of structural economic weaknesses and the social pressures stemming from ongoing economic reforms.

🌱 Very Common