1.95583 leva – Bulgaria

Add to wishlist

Non-circulating coins

Commemoration: Bulgaria in European Union

Bulgaria

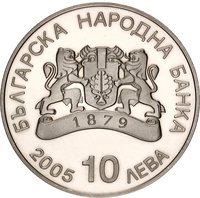

Obverse

Description:

BNB logo and 1879 on strip; issue year 2005 and value.

Inscription:

БЪЛГАРСКА НАРОДНА БАНКА

1879

2005

1.95583 ЛЕВА

1879

2005

1.95583 ЛЕВА

Translation:

BULGARIAN NATIONAL BANK

1879

2005

1.95583 LEVA

1879

2005

1.95583 LEVA

Script: Cyrillic

Language: Bulgarian

Engraver: Bogomil Nikolov

Reverse

Description:

Kazanlak Tomb mural fragment (4th-3rd c. BC) depicting a seated woman, surrounded by 12 gold stars, with "EU", "Bulgaria", and a rose.

Inscription:

EU БЪЛГАРИЯ

Translation:

EU Bulgaria

Script: Cyrillic

Language: Bulgarian

Engraver: Bogomil Nikolov

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Bulgarian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | 14,000 | Proof |

Historical background

In 2005, Bulgaria was operating under a unique and highly successful currency board arrangement, established in 1997 following a severe financial and hyperinflation crisis. This system rigidly fixed the Bulgarian lev (BGN) to the German Deutsche Mark and, after its introduction, to the euro at a rate of 1.95583 leva for 1 euro. The currency board mandated that every lev in circulation be fully backed by foreign reserves, primarily euros, which imposed strict fiscal discipline by eliminating the central bank's ability to print money and finance government deficits. This framework was the cornerstone of Bulgaria's macroeconomic stability throughout the early 2000s, fostering low inflation, restoring public confidence in the national currency, and creating a predictable environment for foreign investment.

The year 2005 was a period of consolidation and anticipation regarding Bulgaria's European Union accession path. The country's economic performance was strong, with robust GDP growth and continued inflows of foreign direct investment. The fixed exchange rate provided stability but also meant that Bulgaria had relinquished independent monetary policy; interest rates effectively mirrored those of the Eurozone. A key focus was maintaining the strict criteria necessary for eventual Eurozone membership, as outlined in the EU's Maastricht Treaty. While not yet a formal member of the Exchange Rate Mechanism (ERM II), the lev's de facto peg to the euro was seen as a preparatory step, with the government expressing its ambition to adopt the euro as soon as possible after EU entry.

However, this rigid system also presented challenges. The currency board limited the Bulgarian National Bank's capacity to act as a lender of last resort, making the banking sector's health critically dependent on effective supervision. Furthermore, the fixed exchange rate could not adjust to correct external imbalances, meaning that competitiveness had to be maintained through internal adjustments like wage and productivity growth rather than currency devaluation. In 2005, these were manageable concerns against a backdrop of strong economic expansion, but they underscored the long-term necessity of structural reforms to ensure a smooth future transition into the Eurozone.

The year 2005 was a period of consolidation and anticipation regarding Bulgaria's European Union accession path. The country's economic performance was strong, with robust GDP growth and continued inflows of foreign direct investment. The fixed exchange rate provided stability but also meant that Bulgaria had relinquished independent monetary policy; interest rates effectively mirrored those of the Eurozone. A key focus was maintaining the strict criteria necessary for eventual Eurozone membership, as outlined in the EU's Maastricht Treaty. While not yet a formal member of the Exchange Rate Mechanism (ERM II), the lev's de facto peg to the euro was seen as a preparatory step, with the government expressing its ambition to adopt the euro as soon as possible after EU entry.

However, this rigid system also presented challenges. The currency board limited the Bulgarian National Bank's capacity to act as a lender of last resort, making the banking sector's health critically dependent on effective supervision. Furthermore, the fixed exchange rate could not adjust to correct external imbalances, meaning that competitiveness had to be maintained through internal adjustments like wage and productivity growth rather than currency devaluation. In 2005, these were manageable concerns against a backdrop of strong economic expansion, but they underscored the long-term necessity of structural reforms to ensure a smooth future transition into the Eurozone.

💎 Very Rare