1 rupee – India

Add to wishlist

Circulating commemorative coins

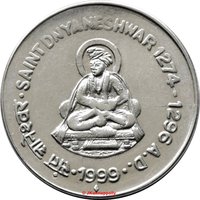

Commemoration: Saint Dnyaneshwar

India

Material

Diameter: 25.1 mm

Weight: 4.85 g

Thickness: 1.4 mm

Shape: Round

Composition: Stainless steel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #2613

Value

Exchange value: 1 INR

Inflation-adjusted value: 4.77 INR

Obverse

Reverse

Edge

Plain or Milled

Mints

| Name | Mark |

|---|---|

| Kolkata / Calcutta / Murshidabad | — |

| Noida | ° |

| Mumbai / Bombay | ♦ |

Historical background

In 1999, India's currency situation was characterized by relative stability under a managed float exchange rate regime, a significant shift from the crisis-driven reforms of the early 1990s. Following the balance of payments crisis in 1991, the Indian Rupee (INR) had moved from a fixed to a market-determined system. By 1999, the Reserve Bank of India (RBI) actively managed volatility within a loose band, intervening to curb excessive fluctuations without targeting a specific level. This period saw the INR trading around ₹43-44 per US Dollar, reflecting a cautious stability amidst emerging market turbulence from the 1997 Asian Financial Crisis.

The macroeconomic backdrop was one of cautious optimism. India had avoided the worst of the Asian crisis due to capital controls and a less exposed financial sector. Foreign exchange reserves, a critical indicator, were steadily rebuilding, crossing the $30 billion mark—a stark contrast to the near-empty coffers of 1991. This reserve cushion provided the RBI greater confidence in managing the currency. However, pressures persisted from a widening current account deficit, fueled by rising oil import bills (the year saw a spike in crude prices) and the economic sanctions imposed after the 1998 nuclear tests, which had constrained foreign investment inflows.

Looking ahead, the currency management in 1999 was setting the stage for future evolution. The focus was on maintaining export competitiveness while controlling inflation, a delicate balancing act. The stability achieved was fragile and heavily reliant on administrative controls and RBI intervention. The period underscored a transitional phase where India was gradually integrating with the global financial system while retaining strong defensive mechanisms, a cautious approach that would define its policy in the early 2000s before moving towards greater liberalization of the capital account.

The macroeconomic backdrop was one of cautious optimism. India had avoided the worst of the Asian crisis due to capital controls and a less exposed financial sector. Foreign exchange reserves, a critical indicator, were steadily rebuilding, crossing the $30 billion mark—a stark contrast to the near-empty coffers of 1991. This reserve cushion provided the RBI greater confidence in managing the currency. However, pressures persisted from a widening current account deficit, fueled by rising oil import bills (the year saw a spike in crude prices) and the economic sanctions imposed after the 1998 nuclear tests, which had constrained foreign investment inflows.

Looking ahead, the currency management in 1999 was setting the stage for future evolution. The focus was on maintaining export competitiveness while controlling inflation, a delicate balancing act. The stability achieved was fragile and heavily reliant on administrative controls and RBI intervention. The period underscored a transitional phase where India was gradually integrating with the global financial system while retaining strong defensive mechanisms, a cautious approach that would define its policy in the early 2000s before moving towards greater liberalization of the capital account.

🌱 Common