½ Rupee – India - British

India

Context

Years: 1905–1910

Country: India

Issuer: India - British

Ruler: Edward VII

Currency:

(1770—1947)

Demonetized: Yes

Total mintage: 16,269,000

Material

References

KM: #Click to copy to clipboard507

Numista: #25488

Value

Bullion value: $15.49

Obverse

Description:

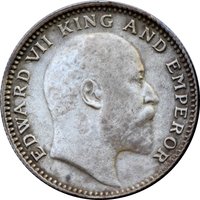

Edward VII bust, right profile

Inscription:

EDWARD VII KING AND EMPEROR

Translation:

EDWARD VII KING AND EMPEROR

Language: English

Engraver: George William de Saulles

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Kolkata / Calcutta / Murshidabad | — |

| Mumbai / Bombay | B |

Mintings

Historical background

In 1905, India's currency system was firmly under the control of the British Raj, operating on a gold-exchange standard established by the Indian Coinage and Paper Currency Act of 1899. The official monetary unit was the Indian Rupee, which was fixed to a sterling exchange rate rather than being directly convertible to gold for the general public. The rupee's value was pegged at 1s 4d (one shilling and four pence), or 15 rupees to the pound sterling. This system aimed to ensure stability for British trade and remittances, tying India's economy closely to London's financial markets.

The currency landscape was a complex duality of metal and paper. Silver coins, including the rupee and its fractions, remained the dominant medium for daily transactions across the vast subcontinent. However, the government issued paper currency notes, which were effectively promises to pay the bearer in "silver rupees" on demand. These notes, managed by the Paper Currency Department, were gaining traction but were still viewed with some suspicion outside major commercial centres. Crucially, the gold standard was maintained through a "council bill" system in London, where sterling could be exchanged for rupees at the fixed rate, ensuring the stability of government finances and facilitating the flow of colonial revenue.

This monetary regime was a source of significant economic tension. It was designed primarily to serve imperial interests, ensuring the smooth extraction of wealth—the "Home Charges"—for payments in London. The fixed high exchange rate (15:1) was often criticised by Indian nationalists and some British officials as overvaluing the rupee, making Indian exports like cotton and jute more expensive on the world market and stifling domestic industrial growth. Furthermore, the system left India vulnerable to global gold market fluctuations and placed the burden of adjustment on the domestic economy, setting the stage for continued financial controversy in the coming decades of the nationalist movement.

The currency landscape was a complex duality of metal and paper. Silver coins, including the rupee and its fractions, remained the dominant medium for daily transactions across the vast subcontinent. However, the government issued paper currency notes, which were effectively promises to pay the bearer in "silver rupees" on demand. These notes, managed by the Paper Currency Department, were gaining traction but were still viewed with some suspicion outside major commercial centres. Crucially, the gold standard was maintained through a "council bill" system in London, where sterling could be exchanged for rupees at the fixed rate, ensuring the stability of government finances and facilitating the flow of colonial revenue.

This monetary regime was a source of significant economic tension. It was designed primarily to serve imperial interests, ensuring the smooth extraction of wealth—the "Home Charges"—for payments in London. The fixed high exchange rate (15:1) was often criticised by Indian nationalists and some British officials as overvaluing the rupee, making Indian exports like cotton and jute more expensive on the world market and stifling domestic industrial growth. Furthermore, the system left India vulnerable to global gold market fluctuations and placed the burden of adjustment on the domestic economy, setting the stage for continued financial controversy in the coming decades of the nationalist movement.

🌱 Fairly Common