100 pesos (Muntinlupa) – Philippines

Add to wishlist

Non-circulating coins

Commemoration: Muntinlupa 100 years

Philippines

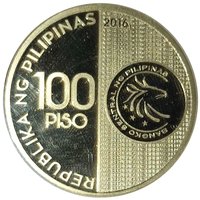

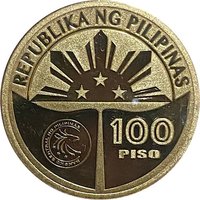

Obverse

Reverse

Description:

Muntinlupa City Hall with centennial logo above and city seal at right.

Inscription:

LAKAS, TALINO AT BUHAY

LUNGSOD NG MULTINLUPA

1917 - 2017

100

TAON

PAPURI SA DIYOS

LUNGSOD NG MULTINLUPA

1917 - 2017

100

TAON

PAPURI SA DIYOS

Translation:

Strength, Intelligence and Life

City of Muntinlupa

1917 - 2017

100

Years

Praise God

City of Muntinlupa

1917 - 2017

100

Years

Praise God

Script: Latin

Language: Tagalog

Edge

Reeded

Categories

| Building |

Mints

| Name | Mark |

|---|---|

| BSP Security Plant Complex | (PI) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | PI | — |

Historical background

In 2017, the Philippine peso (PHP) emerged as one of the worst-performing currencies in Asia, depreciating by approximately 4.5% against the US dollar over the course of the year. This decline was primarily driven by a widening trade deficit, as the country's import growth—fueled by robust domestic demand and infrastructure spending under the government's "Build, Build, Build" program—significantly outpaced export earnings. Furthermore, investor sentiment was periodically dampened by concerns over the country's high inflation rate and the controversial war on drugs, which raised questions about political stability for some international observers.

The Bangko Sentral ng Pilipinas (BSP), the country's central bank, faced a challenging policy environment. To curb inflation and support the peso, the BSP kept its key interest rate at a record low of 3.0% for most of the year but began signaling a shift toward monetary tightening by the fourth quarter. It also intervened directly in the foreign exchange market on several occasions to smooth out excessive volatility. However, these measures were counterbalanced by external pressures, particularly the US Federal Reserve's interest rate hikes and balance sheet normalization, which generally strengthened the US dollar and prompted capital outflows from emerging markets like the Philippines.

Despite the peso's weakness, the broader Philippine economy remained fundamentally strong in 2017, posting a GDP growth rate of 6.7%. The currency depreciation had a dual effect: it increased the cost of servicing the country's dollar-denominated debt and made imports more expensive, contributing to inflation. However, it also provided a boost to the vital Business Process Outsourcing (BPO) sector and families receiving remittances from overseas Filipino workers, as their US dollar earnings translated into more pesos. Thus, the currency situation of 7 reflected a tension between a robust, growing economy and the market pressures stemming from its external imbalances.

The Bangko Sentral ng Pilipinas (BSP), the country's central bank, faced a challenging policy environment. To curb inflation and support the peso, the BSP kept its key interest rate at a record low of 3.0% for most of the year but began signaling a shift toward monetary tightening by the fourth quarter. It also intervened directly in the foreign exchange market on several occasions to smooth out excessive volatility. However, these measures were counterbalanced by external pressures, particularly the US Federal Reserve's interest rate hikes and balance sheet normalization, which generally strengthened the US dollar and prompted capital outflows from emerging markets like the Philippines.

Despite the peso's weakness, the broader Philippine economy remained fundamentally strong in 2017, posting a GDP growth rate of 6.7%. The currency depreciation had a dual effect: it increased the cost of servicing the country's dollar-denominated debt and made imports more expensive, contributing to inflation. However, it also provided a boost to the vital Business Process Outsourcing (BPO) sector and families receiving remittances from overseas Filipino workers, as their US dollar earnings translated into more pesos. Thus, the currency situation of 7 reflected a tension between a robust, growing economy and the market pressures stemming from its external imbalances.

💎 Extremely Rare