10 Rupees – India

Non-circulating coins

Commemoration: FAO - Grow More Food

India

Context

Material

References

KM: #Click to copy to clipboard188

Numista: #22405

Value

Exchange value: 10 INR = $0.11

Bullion value: $32.30

Inflation-adjusted value: 471.90 INR

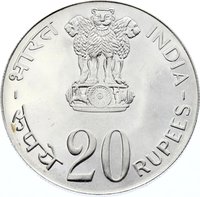

Obverse

Description:

Asoka lion with denomination.

Inscription:

भारत INDIA

10

रूपये RUPEES

10

रूपये RUPEES

Translation:

Ten Rupees

Scripts: Devanagari, Latin

Reverse

Description:

Shield inscribed with grain stalks

Inscription:

अधिक

अन्न

उगाओ

GROW

MORE

FOOD

1973

B

अन्न

उगाओ

GROW

MORE

FOOD

1973

B

Translation:

GROW MORE FOOD

1973

1973

Scripts: Devanagari, Latin

Edge

Reeded

Categories

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| Mumbai / Bombay | ♦ |

| Mumbai / Bombay | B |

Historical background

In 1973, India's currency situation was dominated by the lingering effects of the 1971 Indo-Pakistani War and the subsequent global economic shocks. The war had led to a massive influx of refugees from East Pakistan (now Bangladesh), straining government finances. Furthermore, the breakdown of the Bretton Woods system in 1971, which ended the convertibility of the US dollar to gold, and the 1973 oil price shock created a perfect storm of global monetary instability and soaring import costs. This severely impacted India's balance of payments, putting downward pressure on the rupee's external value.

Domestically, the Indian rupee was officially pegged to the British pound sterling, but its effective exchange rate was managed by the Reserve Bank of India (RBI) against a basket of currencies of major trading partners. To conserve foreign exchange reserves, India maintained a complex system of exchange controls and multiple effective exchange rates for different types of transactions. The year was marked by a significant devaluation, though not in the formal peg. In September 1973, the RBI delinked the rupee from the pound sterling and officially pegged it to the US dollar at a rate of Rs. 7.50 per dollar, which represented a substantial devaluation from the previous effective rate.

This period was characterized by stringent capital controls and a focus on import substitution to safeguard scarce foreign reserves. The economic landscape was one of "financial repression," with the government and RBI directing credit to priority sectors and maintaining a regime of fixed interest rates. The currency measures of 1973, therefore, were less about a free-floating rupee and more about a managed adjustment within a closed, controlled economy, aimed at weathering external crises while supporting the nation's planned development goals.

Domestically, the Indian rupee was officially pegged to the British pound sterling, but its effective exchange rate was managed by the Reserve Bank of India (RBI) against a basket of currencies of major trading partners. To conserve foreign exchange reserves, India maintained a complex system of exchange controls and multiple effective exchange rates for different types of transactions. The year was marked by a significant devaluation, though not in the formal peg. In September 1973, the RBI delinked the rupee from the pound sterling and officially pegged it to the US dollar at a rate of Rs. 7.50 per dollar, which represented a substantial devaluation from the previous effective rate.

This period was characterized by stringent capital controls and a focus on import substitution to safeguard scarce foreign reserves. The economic landscape was one of "financial repression," with the government and RBI directing credit to priority sectors and maintaining a regime of fixed interest rates. The currency measures of 1973, therefore, were less about a free-floating rupee and more about a managed adjustment within a closed, controlled economy, aimed at weathering external crises while supporting the nation's planned development goals.

🌱 Fairly Common