1 Sovereign – United Kingdom

United Kingdom

Context

Years: 1908–1910

Issuer: United Kingdom

Ruler: Edward VII

Currency:

(1158—1970)

Total mintage: 44,921

Material

References

Numista: #22058

Value

Bullion value: $1224.24

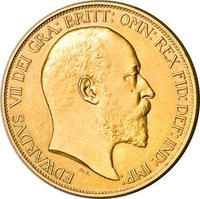

Obverse

Description:

King Edward VII, bareheaded, facing right with surrounding legend.

Inscription:

EDWARDVS VII D: G: BRITT: OMN: REX F: D: IND: IMP:

DeS.

DeS.

Translation:

Edward VII, by the Grace of God, King of all the Britains, Defender of the Faith, Emperor of India.

Script: Latin

Language: Latin

Engraver: George William de Saulles

Reverse

Description:

St. George slaying the dragon on horseback; date and engraver’s initials below. C mintmark above date.

Inscription:

1910

B.P.

B.P.

Script: Latin

Engraver: Benedetto Pistrucci

Edge

Reeded

Categories

| Mythology> Fantastic animal |

| Animal> Horse |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | C |

Historical background

In 1908, the United Kingdom operated under the classical gold standard, a system it had helped pioneer and which underpinned its global financial dominance. The pound sterling was legally defined as a specific weight of gold (0.2354 troy ounces), and Bank of England notes were freely convertible into gold sovereigns or half-sovereigns on demand. This system ensured price stability and immense international confidence in sterling, which functioned as the world's primary reserve and trade currency. The money in circulation was a mix of gold coinage for everyday transactions, supplemented by Bank of England notes (primarily for larger dealings) and a vast network of commercial banknotes issued by trusted Scottish and Irish banks.

However, the period was one of underlying tension and transition. While the gold standard provided stability, it was often criticised for being deflationary and inflexible, tying the money supply to the nation's gold reserves rather than the needs of the domestic economy. Social reformers and emerging Keynesian economists argued that this contributed to persistent unemployment and stifled social spending. Furthermore, the practical use of gold coinage was beginning to wane. The 1908 "Bradbury" committee was established to investigate the feasibility of replacing gold sovereigns with one-pound and ten-shilling treasury notes, signalling a move towards a more fiduciary, paper-based currency while still maintaining the gold anchor.

Ultimately, the currency situation in 1908 represented the peak of the pre-war gold standard's authority, yet it stood on the brink of profound change. The pressures of financing modern government and emerging welfare policies (like the Old Age Pensions Act of 1908) strained the rigid orthodoxy of the system. Within a decade, the financial demands of the First World War would force the UK to suspend gold convertibility, ending this era definitively. Thus, 1908 captures a moment of apparent monetary solidity, quietly harbouring the seeds of its own transformation.

However, the period was one of underlying tension and transition. While the gold standard provided stability, it was often criticised for being deflationary and inflexible, tying the money supply to the nation's gold reserves rather than the needs of the domestic economy. Social reformers and emerging Keynesian economists argued that this contributed to persistent unemployment and stifled social spending. Furthermore, the practical use of gold coinage was beginning to wane. The 1908 "Bradbury" committee was established to investigate the feasibility of replacing gold sovereigns with one-pound and ten-shilling treasury notes, signalling a move towards a more fiduciary, paper-based currency while still maintaining the gold anchor.

Ultimately, the currency situation in 1908 represented the peak of the pre-war gold standard's authority, yet it stood on the brink of profound change. The pressures of financing modern government and emerging welfare policies (like the Old Age Pensions Act of 1908) strained the rigid orthodoxy of the system. Within a decade, the financial demands of the First World War would force the UK to suspend gold convertibility, ending this era definitively. Thus, 1908 captures a moment of apparent monetary solidity, quietly harbouring the seeds of its own transformation.

💎 Very Rare