12.5 euro – Belgium

Add to wishlist

Non-circulating coins

Commemoration: Dynasty of the Belgian kings: Queen Elisabeth.

Belgium

Material

References

KM: #

Numista: #207409

Value

Exchange value: 12.5 EUR

Bullion value: $191.58

Inflation-adjusted value: 16.14 EUR

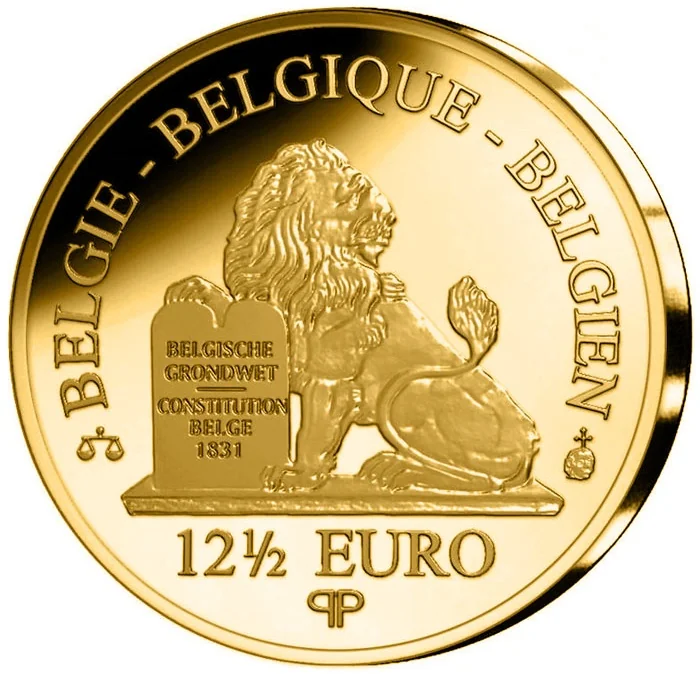

Obverse

Reverse

Edge

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2016 | — | 2,000 | Proof |

Historical background

In 2016, Belgium, as a founding member of the Eurozone, operated exclusively with the euro, which had fully replaced the Belgian franc in 2002. The country's monetary policy was therefore set by the European Central Bank (ECB), with a focus on low inflation and financial stability across the bloc. Domestically, the key monetary issue was the ECB's continuation of its expansive policies, including historically low interest rates and quantitative easing, aimed at stimulating the Eurozone economy in the wake of the sovereign debt crisis. These policies had direct implications for Belgian savers, borrowers, and the government's debt servicing costs.

The domestic financial landscape was marked by a persistent low-interest-rate environment, which pressured bank profitability and offered minimal returns for savers. A significant event was the Belgian government's issuance of a 100-year bond in June 2016, taking advantage of the ultra-low borrowing costs to lock in long-term financing. This reflected a broader strategy of prudent fiscal management, with the government aiming to reduce its public debt-to-GDP ratio, which remained among the highest in Europe at around 106% of GDP.

Beyond the technical monetary setting, public discourse occasionally touched on the broader political dimensions of the single currency. While there was no serious political movement to leave the euro, debates about Eurozone governance, Greek debt relief, and the need for deeper banking and fiscal union were ongoing in Brussels, the de facto capital of the EU. Furthermore, the year was shadowed by the Brexit referendum in June, which created significant uncertainty about the future of European integration and financial markets, indirectly affecting Belgium's highly open and trade-dependent economy.

The domestic financial landscape was marked by a persistent low-interest-rate environment, which pressured bank profitability and offered minimal returns for savers. A significant event was the Belgian government's issuance of a 100-year bond in June 2016, taking advantage of the ultra-low borrowing costs to lock in long-term financing. This reflected a broader strategy of prudent fiscal management, with the government aiming to reduce its public debt-to-GDP ratio, which remained among the highest in Europe at around 106% of GDP.

Beyond the technical monetary setting, public discourse occasionally touched on the broader political dimensions of the single currency. While there was no serious political movement to leave the euro, debates about Eurozone governance, Greek debt relief, and the need for deeper banking and fiscal union were ongoing in Brussels, the de facto capital of the EU. Furthermore, the year was shadowed by the Brexit referendum in June, which created significant uncertainty about the future of European integration and financial markets, indirectly affecting Belgium's highly open and trade-dependent economy.

✨ Legendary