15000 pesos (Jose Maria Cordova) – Colombia

Add to wishlist

Non-circulating coins

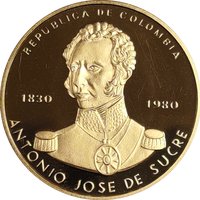

Commemoration: 150th Anniversary of the Death of Jose Maria Cordova

Colombia

Obverse

Reverse

Description:

Coat of arms above country name. Fineness left, weight and metal right. Denomination and year below.

Inscription:

ESCUDO DE LA GRAN COLOMBIA

LEY 0,900

½ ONZA ORO FINO

15000 PESOS

1980

LEY 0,900

½ ONZA ORO FINO

15000 PESOS

1980

Script: Latin

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Event> Death anniversary |

| Symbol> Cornucopia |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1980 | — | 250 |

Historical background

In 1980, Colombia's currency situation was characterized by a managed exchange rate regime within a context of relative macroeconomic stability compared to some of its Latin American neighbors. The country operated under a crawling peg system, where the Colombian peso was periodically devalued against the US dollar at a pre-announced rate. This policy, managed by the Banco de la República, aimed to maintain export competitiveness by offsetting the difference between Colombia's inflation rate (which was in the high teens) and that of its major trading partners, particularly the United States.

This period of relative calm was underpinned by a sustained coffee boom that had begun in the mid-1970s. High international coffee prices generated significant foreign exchange reserves, which bolstered the peso and provided a buffer for the economy. The influx of "café dollars" helped finance imports and allowed the government to avoid the severe balance of payments crises that would soon plague other countries in the region. Consequently, Colombia experienced moderate economic growth and did not resort to the extreme foreign borrowing that led to the Latin American debt crisis.

However, underlying vulnerabilities were present. The economy remained overly dependent on coffee, which accounted for the majority of export earnings, making it susceptible to commodity price shocks. Furthermore, the growth model was beginning to show strains, with inflation persisting as a chronic problem. The stability of 1980 was, therefore, a precarious calm before the storm. By the mid-1980s, a sharp decline in coffee prices, coupled with the regional debt crisis and the growth of illicit drug trade revenues affecting the financial system, would expose these weaknesses and lead to greater exchange rate volatility and economic challenges.

This period of relative calm was underpinned by a sustained coffee boom that had begun in the mid-1970s. High international coffee prices generated significant foreign exchange reserves, which bolstered the peso and provided a buffer for the economy. The influx of "café dollars" helped finance imports and allowed the government to avoid the severe balance of payments crises that would soon plague other countries in the region. Consequently, Colombia experienced moderate economic growth and did not resort to the extreme foreign borrowing that led to the Latin American debt crisis.

However, underlying vulnerabilities were present. The economy remained overly dependent on coffee, which accounted for the majority of export earnings, making it susceptible to commodity price shocks. Furthermore, the growth model was beginning to show strains, with inflation persisting as a chronic problem. The stability of 1980 was, therefore, a precarious calm before the storm. By the mid-1980s, a sharp decline in coffee prices, coupled with the regional debt crisis and the growth of illicit drug trade revenues affecting the financial system, would expose these weaknesses and lead to greater exchange rate volatility and economic challenges.

✨ Legendary