1000 rupees – Nepal

Add to wishlist

Non-circulating coins

Commemoration: Living Goddess Kumari

Nepal

Context

Year: 2000

Vikram Samvat Year:: 2057

Issuer: Nepal

Ruler: Birendra Bir Bikram Shah

Currency:

(since 1932)

Total mintage: 9,000

Material

References

Numista: #190604

Value

Exchange value: 1000 NPR

Bullion value: $97.34

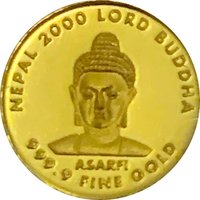

Obverse

Description:

Classic style

Script: Devanagari

Reverse

Scripts: Devanagari, Latin

Edge

Serrated

Mints

| Name | Mark |

|---|---|

| Mint Division of the Central Bank of Nepal | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2000 | — | 9,000 |

Historical background

In the year 2000, Nepal's currency situation was characterized by a stable but tightly controlled exchange rate regime, underpinned by a long-standing peg to the Indian rupee (INR). The Nepalese rupee (NPR) was fixed at a rate of NPR 1.60 = INR 1, a parity maintained since 1993 through the Nepal Rastra Bank (NRB), the country's central bank. This peg provided crucial stability for trade, as India was and remains Nepal's largest trading partner, facilitating cross-border commerce and reducing exchange rate volatility for a significant portion of Nepal's imports and exports. The system was managed under a dual-currency environment in the border region, where the Indian rupee circulated freely alongside the Nepalese rupee.

However, this stability came with significant constraints. The peg necessitated that Nepal's monetary policy closely shadow that of the Reserve Bank of India, limiting the NRB's ability to set independent interest rates or use monetary tools to address domestic economic conditions. Furthermore, the fixed exchange rate exposed the economy to vulnerabilities from India's economic performance and required substantial foreign exchange reserves to defend the parity. By 2000, pressures were emerging from a growing trade deficit with India, which strained forex reserves, and from the need to maintain competitiveness beyond the Indian market.

The broader economic context of 2000 was one of post-conflict uncertainty and low growth, following a decade of political instability. While the currency peg provided an anchor, it also masked underlying structural weaknesses in the economy, including low productivity and a narrow export base beyond hydropower potential and tourism. The fixed exchange rate was thus a double-edged sword: a necessary pillar for economic predictability during a turbulent period, but also a mechanism that limited policy flexibility and highlighted Nepal's deep economic interdependence with its southern neighbor.

However, this stability came with significant constraints. The peg necessitated that Nepal's monetary policy closely shadow that of the Reserve Bank of India, limiting the NRB's ability to set independent interest rates or use monetary tools to address domestic economic conditions. Furthermore, the fixed exchange rate exposed the economy to vulnerabilities from India's economic performance and required substantial foreign exchange reserves to defend the parity. By 2000, pressures were emerging from a growing trade deficit with India, which strained forex reserves, and from the need to maintain competitiveness beyond the Indian market.

The broader economic context of 2000 was one of post-conflict uncertainty and low growth, following a decade of political instability. While the currency peg provided an anchor, it also masked underlying structural weaknesses in the economy, including low productivity and a narrow export base beyond hydropower potential and tourism. The fixed exchange rate was thus a double-edged sword: a necessary pillar for economic predictability during a turbulent period, but also a mechanism that limited policy flexibility and highlighted Nepal's deep economic interdependence with its southern neighbor.

✨ Legendary