1000 pesos uruguayos (Chamber of Commerce) – Uruguay

Add to wishlist

Circulating commemorative coins

Commemoration: 150th. Anniversary of Chamber of Commerce

Uruguay

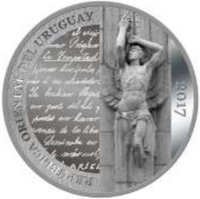

Obverse

Reverse

Description:

Central logo, encircled by event details, with value beneath.

Inscription:

150º Aniversario de la Cámara Nacional de Comercio y Servicios del Uruguay

BOLSA DE COMERCIO

URUGUAY

$ 1.000

BOLSA DE COMERCIO

URUGUAY

$ 1.000

Translation:

150th Anniversary of the National Chamber of Commerce and Services of Uruguay

STOCK EXCHANGE

URUGUAY

$ 1,000

STOCK EXCHANGE

URUGUAY

$ 1,000

Script: Latin

Language: Spanish

Edge

Plain

Categories

| Art> Painting |

| Person> Politician |

| Commerce |

Mints

| Name | Mark |

|---|---|

| Mint of Poland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2017 | — | 1,500 | Proof |

Historical background

In 2017, Uruguay's currency situation was characterized by a period of relative stability and moderate depreciation of the Uruguayan peso (UYU) against the US dollar, following a period of significant volatility in the preceding years. The exchange rate closed the year at approximately 28.7 pesos per dollar, representing a gradual depreciation of about 8% over the course of the year. This controlled weakening was largely managed by the Central Bank of Uruguay (BCU), which had moved away from direct intervention in the foreign exchange market and instead utilized interest rate policy as its primary tool to influence currency flows and contain inflationary pressures.

The economic context for this stability was mixed. While the country continued to face challenges such as a fiscal deficit and inflation persistently above the target range (ending the year at 6.2%), key export sectors like beef, soy, and cellulose remained strong, providing a steady inflow of US dollars. Furthermore, the BCU maintained a substantial level of international reserves, which provided a crucial buffer against external shocks and helped bolster confidence in the peso. This environment allowed the "crawling peg" exchange rate regime to function without major disruptions, permitting a predictable, gradual adjustment.

Overall, 2017 was a year of consolidation for Uruguay's currency, marked by the absence of the sharp swings seen earlier in the decade. The managed depreciation helped maintain the competitiveness of exports, which was vital for the small, open economy. However, underlying structural issues, including the fiscal imbalance and above-target inflation, continued to pose longer-term challenges for monetary and exchange rate policy, setting the stage for ongoing policy debates in the years that followed.

The economic context for this stability was mixed. While the country continued to face challenges such as a fiscal deficit and inflation persistently above the target range (ending the year at 6.2%), key export sectors like beef, soy, and cellulose remained strong, providing a steady inflow of US dollars. Furthermore, the BCU maintained a substantial level of international reserves, which provided a crucial buffer against external shocks and helped bolster confidence in the peso. This environment allowed the "crawling peg" exchange rate regime to function without major disruptions, permitting a predictable, gradual adjustment.

Overall, 2017 was a year of consolidation for Uruguay's currency, marked by the absence of the sharp swings seen earlier in the decade. The managed depreciation helped maintain the competitiveness of exports, which was vital for the small, open economy. However, underlying structural issues, including the fiscal imbalance and above-target inflation, continued to pose longer-term challenges for monetary and exchange rate policy, setting the stage for ongoing policy debates in the years that followed.

💎 Extremely Rare