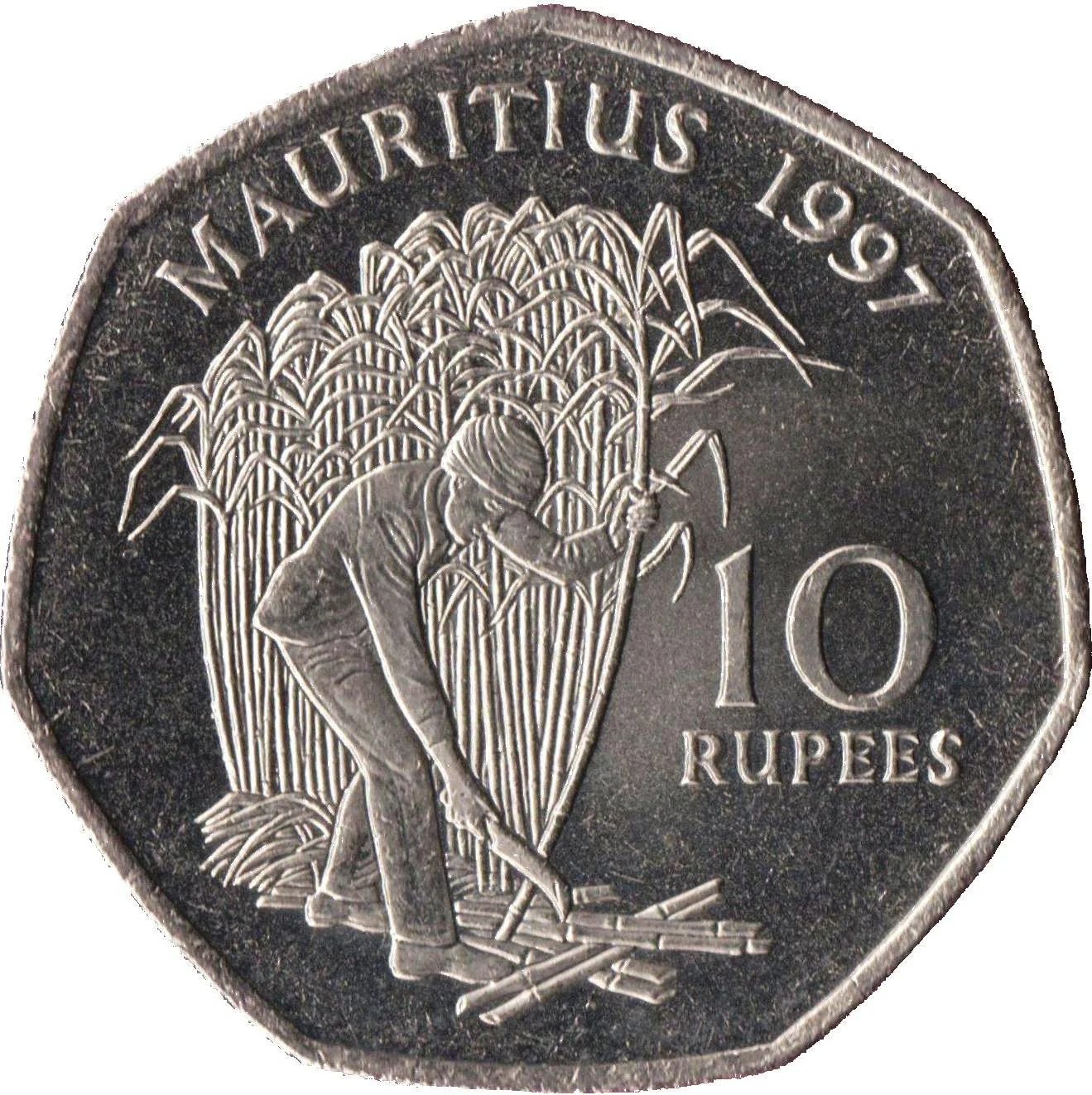

10 rupees – Mauritius

Add to wishlist

Mauritius

Context

Material

Diameter: 27.5 mm

Weight: 10.1 g

Thickness: 2.2 mm

Shape: Equilateral curve heptagon

Composition: Copper-nickel

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #1830

Value

Exchange value: 10 MUR

Obverse

Reverse

Edge

Plain

Categories

| Agriculture |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | — | ||

| 2000 | — | — |

Historical background

In 1997, Mauritius was navigating a period of significant economic transition and vulnerability, with its currency, the Mauritian Rupee (MUR), under managed pressure. The economy, heavily reliant on sugar exports and the burgeoning textile sector, faced external shocks including a decline in global sugar prices and the impending phase-out of preferential trade agreements with the European Union. Concurrently, the Asian Financial Crisis, which erupted in mid-1997, created regional turbulence, leading to capital flight from emerging markets and putting downward pressure on currencies like the rupee. The Bank of Mauritius (BoM) was thus engaged in a delicate balancing act to maintain stability.

The official exchange rate regime was a managed float, but in practice, the BoM maintained a tight peg to a basket of currencies dominated by the British Pound, US Dollar, and French Franc. Throughout 1997, the central bank actively intervened in the foreign exchange market to defend the rupee, drawing on its reserves to curb excessive volatility and prevent a sharp depreciation. This defensive stance was costly and aimed at controlling imported inflation and maintaining investor confidence during a uncertain global climate, though it limited monetary policy autonomy.

Ultimately, the pressures of 1997 highlighted structural economic vulnerabilities and contributed to a policy shift in the following years. The sustained defense of the currency strained foreign reserves and underscored the need for greater exchange rate flexibility to absorb external shocks. This experience paved the way for a more liberalized foreign exchange market in the early 2000s, where the rupee moved towards a more market-driven valuation while the central bank retained the role of smoothing disorderly fluctuations.

The official exchange rate regime was a managed float, but in practice, the BoM maintained a tight peg to a basket of currencies dominated by the British Pound, US Dollar, and French Franc. Throughout 1997, the central bank actively intervened in the foreign exchange market to defend the rupee, drawing on its reserves to curb excessive volatility and prevent a sharp depreciation. This defensive stance was costly and aimed at controlling imported inflation and maintaining investor confidence during a uncertain global climate, though it limited monetary policy autonomy.

Ultimately, the pressures of 1997 highlighted structural economic vulnerabilities and contributed to a policy shift in the following years. The sustained defense of the currency strained foreign reserves and underscored the need for greater exchange rate flexibility to absorb external shocks. This experience paved the way for a more liberalized foreign exchange market in the early 2000s, where the rupee moved towards a more market-driven valuation while the central bank retained the role of smoothing disorderly fluctuations.

🌱 Very Common