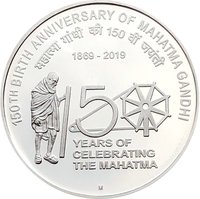

150 rupees (Mahatma Gandhi) – India

Add to wishlist

Non-circulating coins

Commemoration: 150th Birth Anniversary of Mahatma Gandhi

India

Material

References

KM: #

Numista: #181088

Value

Exchange value: 150 INR

Bullion value: $98.92

Inflation-adjusted value: 213.05 INR

Obverse

Reverse

Description:

Logo for Gandhi's 150th Birth Anniversary

Inscription:

150th Birth Anniversary of Mahatma Gandhi

1869 - 2019

1869 - 2019

Edge

200 Serrations

Mints

| Name | Mark |

|---|---|

| Mumbai / Bombay | ♦ |

| Mumbai / Bombay | M |

Historical background

In 2019, India's currency situation was characterized by relative stability and ongoing efforts to manage liquidity following the significant structural shocks of the previous years, most notably the 2016 demonetization. The Indian Rupee (INR) traded in a managed float, with the Reserve Bank of India (RBI) actively intervening in foreign exchange markets to curb excessive volatility. Throughout the year, the rupee faced moderate depreciation pressure, averaging around 71 against the US dollar, influenced by global factors like rising oil prices and persistent trade deficits, alongside domestic challenges such as a slowdown in economic growth and some stress in the non-banking financial company (NBFC) sector.

A key focus for monetary authorities was addressing the liquidity crunch that had emerged in the financial system. The RBI undertook several measures, including open market operations (OMOs) and a reduction in the repo rate by 135 basis points over the year in a shift to an accommodative stance. This aimed to stimulate credit growth and support the economy. However, the transmission of these rate cuts to end borrowers remained inefficient, limiting their full impact. The government also continued to promote digital payments and financial inclusion as part of a broader strategy to formalize the economy.

Overall, 2019 was a year of cautious management rather than dramatic reform. The currency market was stable but watchful, with the RBI balancing objectives of controlling inflation, supporting growth, and maintaining foreign exchange reserves. The period set the stage for the more profound economic upheaval that would follow in early 2020 with the onset of the COVID-19 pandemic, which would necessitate a new set of emergency monetary and fiscal responses.

A key focus for monetary authorities was addressing the liquidity crunch that had emerged in the financial system. The RBI undertook several measures, including open market operations (OMOs) and a reduction in the repo rate by 135 basis points over the year in a shift to an accommodative stance. This aimed to stimulate credit growth and support the economy. However, the transmission of these rate cuts to end borrowers remained inefficient, limiting their full impact. The government also continued to promote digital payments and financial inclusion as part of a broader strategy to formalize the economy.

Overall, 2019 was a year of cautious management rather than dramatic reform. The currency market was stable but watchful, with the RBI balancing objectives of controlling inflation, supporting growth, and maintaining foreign exchange reserves. The period set the stage for the more profound economic upheaval that would follow in early 2020 with the onset of the COVID-19 pandemic, which would necessitate a new set of emergency monetary and fiscal responses.

⭐ Somewhat Rare