3 Rubles (EAEU) – Russian Federation

Non-circulating coins

Commemoration: 5th Anniversary of the EAEU

Russia

Context

Year: 2019

Country: Russia

Issuer: Russian Federation

Period:

(since 1991)

Currency:

(since 1998)

Total mintage: 3,000

Material

References

Value

Exchange value: 3 RUB

Bullion value: $89.85

Inflation-adjusted value: 5.51 RUB

Obverse

Description:

The obverse features the Russian Federation coat of arms with the country name above. Below are the metal specifications, mint mark, and the inscriptions "BANK OF RUSSIA," "3 ROUBLES," and the year.

Inscription:

РОССИЙСКАЯ ФЕДЕРАЦИЯ

Ag 925 31,1

СПМД

БАНК РОССИИ

3 РУБЛЯ

2019 г.

Ag 925 31,1

СПМД

БАНК РОССИИ

3 РУБЛЯ

2019 г.

Translation:

RUSSIAN FEDERATION

Ag 925 31.1

SPMD

BANK OF RUSSIA

3 RUBLES

2019

Ag 925 31.1

SPMD

BANK OF RUSSIA

3 RUBLES

2019

Language: Russian

Engraver: Alexandra Arsenyevna Dolgopolova

Designer: Elena Viktorovna Kramskaya

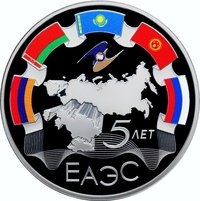

Reverse

Description:

Central EAEU member silhouettes, with their national flags arching above and curving downward around the EAEU emblem. "5 ЛЕТ" and "ЕАЭС" are at the bottom.

Inscription:

5

ЛЕТ

ЕАЭС

ЛЕТ

ЕАЭС

Translation:

5 Years of the EAEU

Script: Cyrillic

Language: Russian

Designer: Sergey Vladilenovich Sutyagin

Edge

300 corrugations

Mints

| Name | Mark |

|---|---|

| Saint Petersburg | (СПМД) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2019 | СПМД | 3,000 | Proof |

Historical background

In 2019, the Russian ruble (RUB) demonstrated notable stability and even modest strength, a significant shift from the volatility experienced earlier in the decade. This relative calm was primarily anchored by two key factors: conservative fiscal policy and supportive external conditions. The Russian Ministry of Finance continued its "budget rule," which automatically channels excess oil revenues into the National Wealth Fund when prices exceed a set baseline, insulating the domestic economy and currency from commodity price swings. Concurrently, the Central Bank of Russia maintained a consistent tight monetary policy, with a key interest rate of 7.75% at year's end, which helped control inflation and made ruble-denominated assets attractive.

The external environment was broadly favorable. Global oil prices, while not at peak levels, remained relatively firm, with the Brent crude benchmark averaging around $64 per barrel for the year. This provided a steady flow of export revenues, supporting the country's current account surplus. Furthermore, the absence of major new international sanctions—following the significant rounds imposed in 2014 and 2018—removed a key source of downward pressure and investor uncertainty. The ruble's performance was also aided by a generally weaker US dollar in global markets during parts of the year.

However, underlying vulnerabilities persisted beneath the surface stability. The economy continued to face structural challenges, including low growth potential, limited foreign investment due to geopolitical tensions, and susceptibility to any future downturn in energy markets. Inflation, though controlled, ended the year at 3%, slightly above the Central Bank's target. Overall, 2019 represented a year of consolidation for the ruble, where prudent domestic policies and a benign external climate allowed it to recover from previous shocks, yet without resolving the longer-term dependencies and risks inherent in the Russian economic model.

The external environment was broadly favorable. Global oil prices, while not at peak levels, remained relatively firm, with the Brent crude benchmark averaging around $64 per barrel for the year. This provided a steady flow of export revenues, supporting the country's current account surplus. Furthermore, the absence of major new international sanctions—following the significant rounds imposed in 2014 and 2018—removed a key source of downward pressure and investor uncertainty. The ruble's performance was also aided by a generally weaker US dollar in global markets during parts of the year.

However, underlying vulnerabilities persisted beneath the surface stability. The economy continued to face structural challenges, including low growth potential, limited foreign investment due to geopolitical tensions, and susceptibility to any future downturn in energy markets. Inflation, though controlled, ended the year at 3%, slightly above the Central Bank's target. Overall, 2019 represented a year of consolidation for the ruble, where prudent domestic policies and a benign external climate allowed it to recover from previous shocks, yet without resolving the longer-term dependencies and risks inherent in the Russian economic model.

✨ Legendary