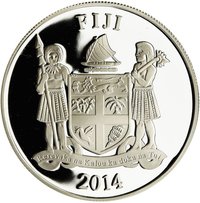

100 Dollars – Fiji

Fiji

Context

Material

Diameter: 100 mm

Weight: 1000 g

Silver weight: 999.00 g

Shape: Round

Composition: 99.9% Silver

Standard: Silver kilo

Magnetic: No

References

Numista: #174780

Value

Exchange value: 100 FJD

Bullion value: $2839.86

Obverse

Reverse

Edge

Plain

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2014 | — | 100 |

Historical background

In 2014, Fiji's currency situation was characterized by a period of relative stability and strategic management under the Reserve Bank of Fiji (RBF). Following the global financial crisis and a series of domestic devaluations in 2009 and 2011, the Fijian dollar (FJD) had settled into a managed float regime. The RBF's primary objective was to maintain adequate foreign reserves, which had recovered to comfortable levels above the benchmark of four months of import cover. This stability was crucial for supporting economic confidence and financing essential imports, particularly as the country continued its recovery from the 2009 political crisis and aimed for democratic elections later in the year.

The central bank's policy focused on maintaining a competitive exchange rate to bolster key export sectors like tourism and sugar, while also controlling inflationary pressures. Inflation, which had spiked following the 2011 devaluation, was moderating and ended the year at around 1.2%. The RBF employed a combination of monetary policy tools, including a low interest rate environment (the Overnight Policy Rate was held at 0.5%) to stimulate investment, alongside direct intervention in the foreign exchange market to smooth volatility. This careful balancing act aimed to support economic growth without jeopardizing reserve levels or price stability.

Overall, 2014 represented a year of consolidation for Fiji's currency. The stable exchange rate, controlled inflation, and robust foreign reserves provided a favorable macroeconomic backdrop for the historic September 2014 general election, which restored parliamentary democracy. This stability was seen as a foundation for the anticipated post-election economic boost, encouraging investment and setting the stage for the stronger growth periods that followed. The RBF's successful management during this transitional year helped reinforce the Fijian dollar's credibility.

The central bank's policy focused on maintaining a competitive exchange rate to bolster key export sectors like tourism and sugar, while also controlling inflationary pressures. Inflation, which had spiked following the 2011 devaluation, was moderating and ended the year at around 1.2%. The RBF employed a combination of monetary policy tools, including a low interest rate environment (the Overnight Policy Rate was held at 0.5%) to stimulate investment, alongside direct intervention in the foreign exchange market to smooth volatility. This careful balancing act aimed to support economic growth without jeopardizing reserve levels or price stability.

Overall, 2014 represented a year of consolidation for Fiji's currency. The stable exchange rate, controlled inflation, and robust foreign reserves provided a favorable macroeconomic backdrop for the historic September 2014 general election, which restored parliamentary democracy. This stability was seen as a foundation for the anticipated post-election economic boost, encouraging investment and setting the stage for the stronger growth periods that followed. The RBF's successful management during this transitional year helped reinforce the Fijian dollar's credibility.

✨ Legendary