20 hryven (National Academy of Sciences of Ukraine) – Ukraine

Add to wishlist

Non-circulating coins

Commemoration: 100th Anniversary of the National Academy of Sciences of Ukraine

Ukraine

Context

Year: 2018

Issuer: Ukraine

Issuing organization: National Bank of Ukraine

Period:

(since 1991)

Currency:

(since 1996)

Total mintage: 2,500

Material

References

KM: #

Numista: #154935

Value

Exchange value: 20 UAH

Bullion value: $152.12

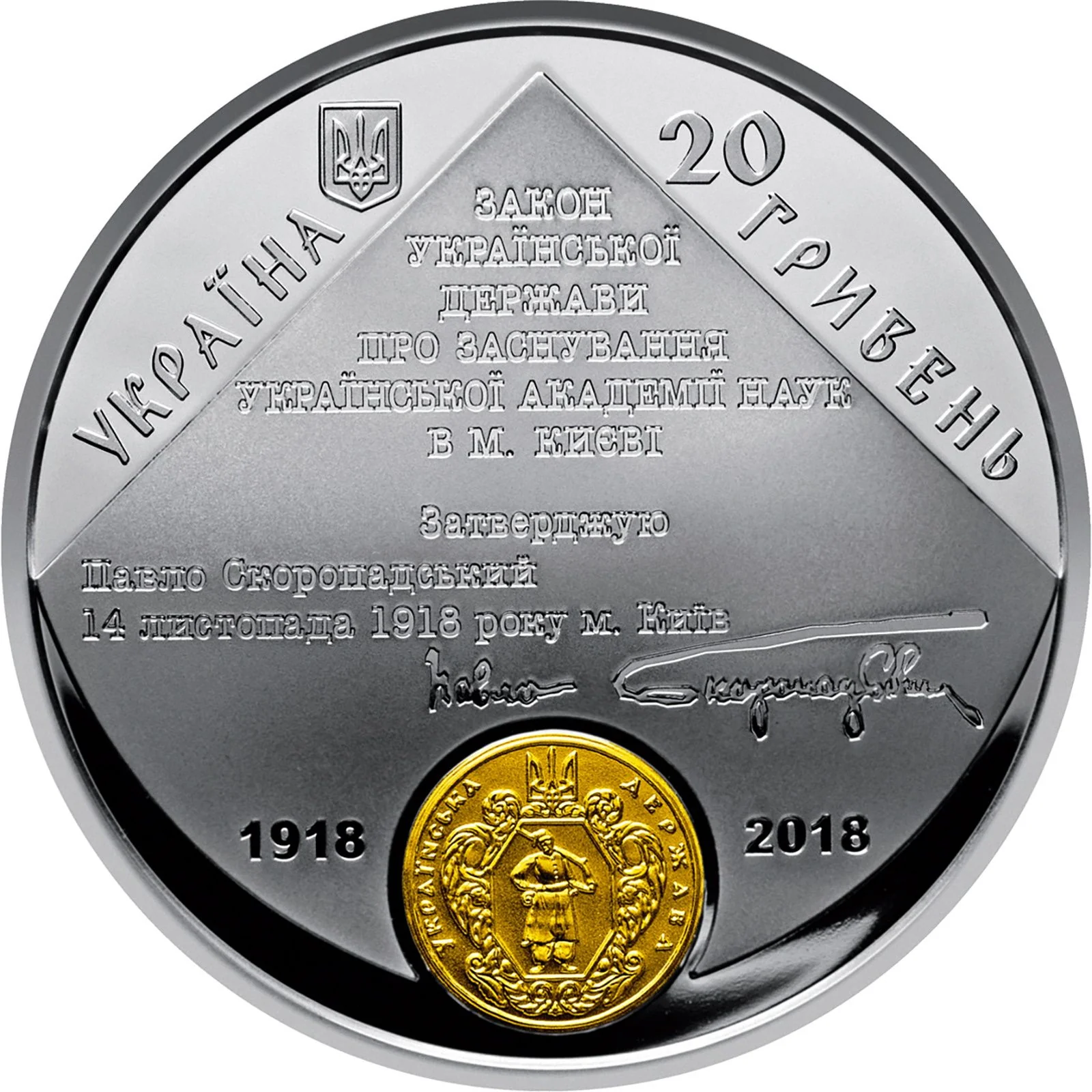

Obverse

Description:

Ukraine’s small coat of arms and the word "УКРАЇНА" are at the top left; the face value "20 ГРИВЕНЬ" is at the top right. Centered on a matt background is the text of the law establishing the Ukrainian Academy of Sciences in Kyiv, approved by Pavlo Skoropadskyi on 14 November 1918, followed by his facsimile signature. Below is the gilt stamp of the Ukrainian state, flanked by the years 1918 and 2018.

Inscription:

УКРАЇНА

20 ГРИВЕНЬ

1918 2018

20 ГРИВЕНЬ

1918 2018

Translation:

UKRAINE

20 HRYVEN

1918 2018

20 HRYVEN

1918 2018

Scripts: Cyrillic, Cyrillic (cursive)

Language: Ukrainian

Engravers: Volodymyr Demianenko, Sviatoslav Ivanenko

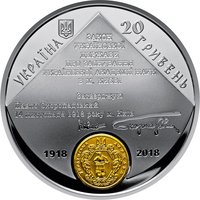

Reverse

Description:

The yellow Presidium building is centered, topped with "100/РОКІВ." A circle of portraits and signatures of past presidents surrounds it: Vernadskyi (top), Levytskyi (right), Vasylenko (left), Lypskyi (left), Zabolotnyi (right), Bohomolets (bottom left), Palladin (bottom right), and Paton (bottom center). Below on a matte background is "НАЦІОНАЛЬНА/АКАДЕМІЯ НАУК/УКРАЇНИ."

Inscription:

100 РОКІВ

НАЦІОНАЛЬНА АКАДЕМІЯ НАУК УКРАЇНИ

НАЦІОНАЛЬНА АКАДЕМІЯ НАУК УКРАЇНИ

Translation:

100 Years

National Academy of Sciences of Ukraine

National Academy of Sciences of Ukraine

Script: Cyrillic

Language: Ukrainian

Engravers: Volodymyr Demianenko, Sviatoslav Ivanenko

Edge

Smooth with in-depth legends

Legend:

Ag 925 62,2

Categories

| Science |

| Building |

| Currency> Stamp depiction |

| Education |

Mints

| Name | Mark |

|---|---|

| National Bank of Ukraine Banknote Printing and Minting Works | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2018 | — | 2,500 | Proof |

Historical background

In 2018, Ukraine's currency, the hryvnia (UAH), demonstrated remarkable stability, a significant achievement following the severe economic and currency crisis of 2014-2015. During that earlier period, the hryvnia had lost nearly 70% of its value against the US dollar due to the combined shocks of the Russian annexation of Crimea, war in the Donbas region, collapsing exports, and a loss of foreign reserves. By 2018, however, the National Bank of Ukraine (NBU) had successfully implemented a managed floating exchange rate regime, supported by a crucial $17.5 billion International Monetary Fund (IMF) program. This stability was underpinned by consistent foreign currency inflows from robust agricultural exports, steady remittances from workers abroad, and improved investor confidence due to ongoing, though often slow, reform efforts.

The central bank's primary focus in 2018 was on building foreign exchange reserves and maintaining tight monetary policy to control inflation. After dipping below $5 billion in early 2015, Ukraine's international reserves were steadily rebuilt, reaching a five-year high of over $20 billion by the end of 2018. This buffer provided crucial protection against external shocks. Furthermore, the NBU maintained a high discount rate (18% for most of the year) to curb inflationary pressures, which had spiked to over 60% in 2015 but were brought down to a single-digit annual rate by late 2018. This combination of factors allowed the hryvnia to trade within a relatively narrow corridor of around UAH 27-28 per US dollar throughout the year.

Despite this surface stability, underlying vulnerabilities persisted. The economy remained heavily dependent on volatile commodity exports, particularly steel and grain. Structural reforms in areas like the judiciary and state-owned enterprises, which were key to unlocking further IMF tranches and sustaining long-term confidence, faced significant political resistance and delays. Consequently, while 2018 represented a year of hard-won monetary stabilization and a pause from crisis, it was a stability that remained fragile and contingent on continued external financial support and the politically difficult implementation of deeper economic reforms.

The central bank's primary focus in 2018 was on building foreign exchange reserves and maintaining tight monetary policy to control inflation. After dipping below $5 billion in early 2015, Ukraine's international reserves were steadily rebuilt, reaching a five-year high of over $20 billion by the end of 2018. This buffer provided crucial protection against external shocks. Furthermore, the NBU maintained a high discount rate (18% for most of the year) to curb inflationary pressures, which had spiked to over 60% in 2015 but were brought down to a single-digit annual rate by late 2018. This combination of factors allowed the hryvnia to trade within a relatively narrow corridor of around UAH 27-28 per US dollar throughout the year.

Despite this surface stability, underlying vulnerabilities persisted. The economy remained heavily dependent on volatile commodity exports, particularly steel and grain. Structural reforms in areas like the judiciary and state-owned enterprises, which were key to unlocking further IMF tranches and sustaining long-term confidence, faced significant political resistance and delays. Consequently, while 2018 represented a year of hard-won monetary stabilization and a pause from crisis, it was a stability that remained fragile and contingent on continued external financial support and the politically difficult implementation of deeper economic reforms.

✨ Legendary