1 dirham (Zakum Development Company) – United Arab Emirates

Add to wishlist

Circulating commemorative coins

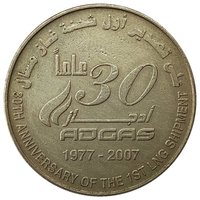

Commemoration: The 30th Anniversary of Zakum Development Company (ZADCO) in the Emirate of Abu Dhabi

United Arab Emirates

Context

Year: 2007

Issuer: United Arab Emirates

Ruler: Khalifa bin Zayed Al Nahyan

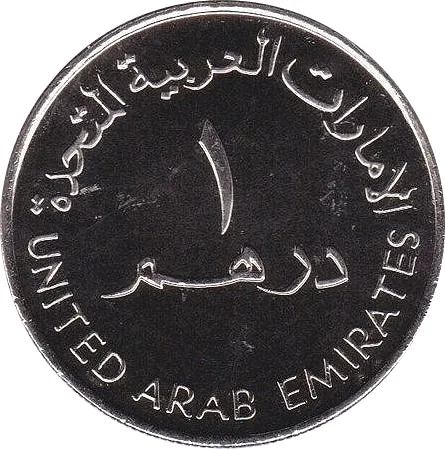

Currency:

(since 1973)

Total mintage: 250,000

Material

Diameter: 23.8 mm

Weight: 6.4 g

Thickness: 1.9 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #15470

Value

Exchange value: 1 AED

Obverse

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | — | 250,000 |

Historical background

In 2007, the currency situation in the United Arab Emirates was defined by its long-standing peg to the US dollar, a policy established in the late 1970s. This fixed exchange rate of approximately 3.6725 UAE dirhams to one US dollar provided crucial stability for the nation's oil-dominated economy, as global oil prices were (and still are) denominated in dollars. The peg also fostered a predictable environment for trade and foreign investment, which was particularly vital as the UAE, especially Dubai, was experiencing an unprecedented real estate and construction boom fueled by significant international capital inflows.

However, this period also exposed the key drawback of the dollar peg: imported inflation. With the US Federal Reserve cutting interest rates in response to the emerging subprime mortgage crisis, the UAE's monetary policy was effectively forced to follow suit to maintain the peg, despite its own overheating economy. This led to interest rates that were too low for local conditions, exacerbating asset price inflation. Furthermore, as the dollar weakened against other major currencies throughout 2007, the dirham also depreciated in tandem, making imports from Europe and Asia more expensive and contributing to a sharp rise in domestic inflation, which reached a record high.

Consequently, 2007 was a year of intense debate and speculation about a potential revaluation or even a de-pegging of the dirham. Pressure mounted from within the Gulf Cooperation Council (GCC), as the planned single currency project faced hurdles, and other member states like Kuwait had already abandoned their strict dollar peg. While the UAE Central Bank repeatedly reaffirmed its commitment to the dollar peg as a cornerstone of monetary stability, the economic tensions of 7 laid the groundwork for the serious reconsideration that would follow in the coming years.

However, this period also exposed the key drawback of the dollar peg: imported inflation. With the US Federal Reserve cutting interest rates in response to the emerging subprime mortgage crisis, the UAE's monetary policy was effectively forced to follow suit to maintain the peg, despite its own overheating economy. This led to interest rates that were too low for local conditions, exacerbating asset price inflation. Furthermore, as the dollar weakened against other major currencies throughout 2007, the dirham also depreciated in tandem, making imports from Europe and Asia more expensive and contributing to a sharp rise in domestic inflation, which reached a record high.

Consequently, 2007 was a year of intense debate and speculation about a potential revaluation or even a de-pegging of the dirham. Pressure mounted from within the Gulf Cooperation Council (GCC), as the planned single currency project faced hurdles, and other member states like Kuwait had already abandoned their strict dollar peg. While the UAE Central Bank repeatedly reaffirmed its commitment to the dollar peg as a cornerstone of monetary stability, the economic tensions of 7 laid the groundwork for the serious reconsideration that would follow in the coming years.

🌱 Common