25 Tala – Samoa

Non-circulating coins

Commemoration: America's Cup

Samoa

Material

Diameter: 65 mm

Weight: 155.52 g

Silver weight: 155.36 g

Shape: Round

Composition: 99.9% Silver

Standard: Silver 5 ounces

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard67

Numista: #104958

Value

Exchange value: 25 WST

Bullion value: $451.34

Obverse

Description:

America's Cup within beaded circle above value.

Inscription:

SAMOA I SISIFO

FIVE OUNCES · $25 · .999 SILVER

FIVE OUNCES · $25 · .999 SILVER

Script: Latin

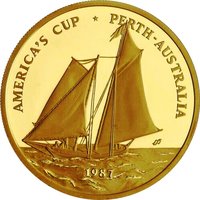

Reverse

Description:

Sailing ship logo above date.

Inscription:

AMERICA'S CUP · PERTH - AUSTRALIA

1987

1987

Script: Latin

Edge

Reeded

Categories

| Transportation> Watercraft |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1987 | — | — | Proof |

Historical background

In 1987, Samoa (then known as Western Samoa) faced a significant currency crisis rooted in its fixed exchange rate system. The Samoan tala was pegged to a basket of currencies, heavily weighted towards the New Zealand dollar. This link became problematic as the New Zealand dollar depreciated sharply in the mid-1980s following major economic reforms and the 1985 float of its currency. Consequently, the tala was pulled down in value against other major currencies like the US dollar and the Australian dollar, despite Samoa's own economic conditions. This misalignment made imports, particularly essential goods, machinery, and petroleum, prohibitively expensive, fueling inflation and straining the nation's foreign reserves.

The government, led by Prime Minister Tofilau Eti Alesana, was confronted with a difficult choice: continue depleting reserves to defend the unsustainable peg or implement a politically risky devaluation. After careful consideration, the decision was made to devalue the tala by approximately 33% in September 1987. This decisive move aimed to correct the external imbalance, curb the drain on reserves, and restore competitiveness to the country's agricultural exports, chiefly coconuts, cocoa, and taro. The devaluation was part of a broader structural adjustment program supported by the International Monetary Fund and the World Bank.

The immediate aftermath of the 1987 devaluation was challenging for the Samoan populace, as the cost of living increased sharply. However, the adjustment is generally viewed by economists as a necessary corrective measure that laid the groundwork for greater macroeconomic stability in the following decades. It marked a pivotal moment in Samoa's financial history, moving the country toward a more realistic and managed exchange rate framework that better reflected its economic fundamentals and trading relationships, ultimately reducing its vulnerability to external shocks from a single partner nation.

The government, led by Prime Minister Tofilau Eti Alesana, was confronted with a difficult choice: continue depleting reserves to defend the unsustainable peg or implement a politically risky devaluation. After careful consideration, the decision was made to devalue the tala by approximately 33% in September 1987. This decisive move aimed to correct the external imbalance, curb the drain on reserves, and restore competitiveness to the country's agricultural exports, chiefly coconuts, cocoa, and taro. The devaluation was part of a broader structural adjustment program supported by the International Monetary Fund and the World Bank.

The immediate aftermath of the 1987 devaluation was challenging for the Samoan populace, as the cost of living increased sharply. However, the adjustment is generally viewed by economists as a necessary corrective measure that laid the groundwork for greater macroeconomic stability in the following decades. It marked a pivotal moment in Samoa's financial history, moving the country toward a more realistic and managed exchange rate framework that better reflected its economic fundamentals and trading relationships, ultimately reducing its vulnerability to external shocks from a single partner nation.

💎 Extremely Rare