25 Schilling (Lukas von Hildebrandt) – Austria

Non-circulating coins

Commemoration: 300th Anniversary of birth of Lukas von Hildebrandt

Austria

Obverse

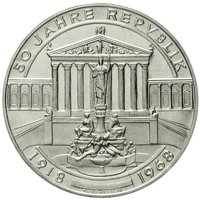

Reverse

Description:

Belvedere Castle entrance

Inscription:

1668 LUKAS VON HILDEBRANDT 1745

BELVEDERE

1968

BELVEDERE

1968

Script: Latin

Engraver: Kurt Bodlak

Edge

Smooth with value

Legend:

FUENFUNDZWANZIG SCHILLING **

Translation:

Twenty-Five Schilling

Language: German

Categories

| Building> Castle or fortification |

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Münze Österreich | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1968 | — | 1,258,000 | ||

| 1968 | — | 42,000 | Proof |

Historical background

In 1968, Austria operated under a stable and successful hard currency policy, a cornerstone of its post-war economic identity. The Austrian schilling, reintroduced in 1945, was firmly pegged to the US dollar at a fixed rate of 26 schillings to 1 dollar, a parity established in 1953. This commitment to a strong, convertible currency, managed by the respected Oesterreichische Nationalbank (OeNB), was a deliberate political and economic choice. It fostered low inflation, attracted foreign investment, and symbolized the country's economic recovery and integration into the Western bloc, contrasting sharply with the controlled currencies of Eastern Europe.

This stability, however, existed within a tense international monetary environment. The Bretton Woods system of fixed exchange rates was under growing strain due to US balance-of-payments deficits and inflationary pressures. While not at the epicenter of the crises that would eventually unravel the system, Austria was keenly aware of the vulnerabilities. The schilling's dollar peg meant that international turbulence, particularly speculation against the dollar or the Deutsche Mark (a key reference currency for Austria's trade), required vigilant management by the OeNB to maintain the agreed parity and domestic price stability.

Domestically, 1968 was a year of robust economic growth and near-full employment, which validated the hard currency policy in the public eye. There were no major currency reforms or devaluations that year; the story was one of continuity and confidence. The social partnership, Austria's unique system of consensus between government, business, and labor unions, strongly supported this policy, accepting that wage moderation was necessary to maintain the schilling's strength and Austria's export competitiveness. Thus, the currency situation in 1968 was characterized by a successful, defensive adherence to a fixed parity, providing a bedrock of stability while the foundations of the global monetary order began to shake.

This stability, however, existed within a tense international monetary environment. The Bretton Woods system of fixed exchange rates was under growing strain due to US balance-of-payments deficits and inflationary pressures. While not at the epicenter of the crises that would eventually unravel the system, Austria was keenly aware of the vulnerabilities. The schilling's dollar peg meant that international turbulence, particularly speculation against the dollar or the Deutsche Mark (a key reference currency for Austria's trade), required vigilant management by the OeNB to maintain the agreed parity and domestic price stability.

Domestically, 1968 was a year of robust economic growth and near-full employment, which validated the hard currency policy in the public eye. There were no major currency reforms or devaluations that year; the story was one of continuity and confidence. The social partnership, Austria's unique system of consensus between government, business, and labor unions, strongly supported this policy, accepting that wage moderation was necessary to maintain the schilling's strength and Austria's export competitiveness. Thus, the currency situation in 1968 was characterized by a successful, defensive adherence to a fixed parity, providing a bedrock of stability while the foundations of the global monetary order began to shake.

🌱 Common