10 Markkaa (Independence) – Finland

Non-circulating coins

Commemoration: 60th Anniversary of Independence

Finland

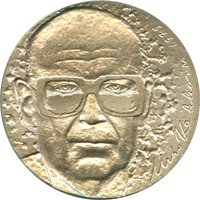

Obverse

Description:

Four-line inscription over five-line, date at right.

Inscription:

ITSENAÏNEN SUOMI YHTEINEN ASIAMME

1917-1977

1917-1977

Translation:

OUR FINLAND INDEPENDENT OUR CAUSE COMMON

1917-1977

1917-1977

Script: Latin

Language: Finnish

Engraver: Heikki Häiväoja

Reverse

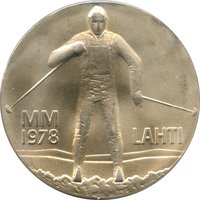

Description:

Denomination upper right.

Inscription:

10

MARKKAA

MARK

K H

MARKKAA

MARK

K H

Script: Latin

Engraver: Heikki Häiväoja

Edge

Plain

Categories

| Event> Independence |

Mints

| Name | Mark |

|---|---|

| Mint of Finland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1977 | H | 383,000 |

Historical background

In 1977, Finland's currency situation was defined by its membership in the Nordic Currency Union (with Sweden, Denmark, and Norway), a system that had officially ended in 1924 but whose legacy continued through a fixed exchange rate peg. The Finnish markka (FIM) was tightly pegged to a trade-weighted basket of currencies, primarily reflecting the value of the Soviet ruble, the German Deutsche Mark, and the Swedish krona. This "basket peg" was a cornerstone of Finland's economic policy, designed to provide stability for its heavily export-dependent economy, which relied on both Western markets and significant bilateral trade with the Soviet Union.

Domestically, this period was marked by the aftermath of the 1973 oil crisis and a series of competitive devaluations. To maintain export competitiveness amid global inflation and rising costs, Finland had devalued the markka in 1967 and again in 1977 itself. The devaluation of 1977, by approximately 5.6%, was a deliberate policy tool to boost Finnish exports by making them cheaper abroad, while also addressing a growing current account deficit. However, this came at the cost of making imports more expensive, contributing to domestic inflation.

Overall, the currency regime in 1977 was one of managed stability with strategic interventions. The Bank of Finland actively maintained the peg through foreign exchange controls and market operations. While successful in providing a predictable framework for trade, the system was inherently rigid, limiting independent monetary policy and making the economy vulnerable to external shocks. This period represented the later stages of the Bretton Woods era's influence, preceding the financial deregulation and eventual float of the markka that would occur in the early 1990s.

Domestically, this period was marked by the aftermath of the 1973 oil crisis and a series of competitive devaluations. To maintain export competitiveness amid global inflation and rising costs, Finland had devalued the markka in 1967 and again in 1977 itself. The devaluation of 1977, by approximately 5.6%, was a deliberate policy tool to boost Finnish exports by making them cheaper abroad, while also addressing a growing current account deficit. However, this came at the cost of making imports more expensive, contributing to domestic inflation.

Overall, the currency regime in 1977 was one of managed stability with strategic interventions. The Bank of Finland actively maintained the peg through foreign exchange controls and market operations. While successful in providing a predictable framework for trade, the system was inherently rigid, limiting independent monetary policy and making the economy vulnerable to external shocks. This period represented the later stages of the Bretton Woods era's influence, preceding the financial deregulation and eventual float of the markka that would occur in the early 1990s.

🌱 Fairly Common