1 Baht (World Health Organization) – Thailand

Circulating commemorative coins

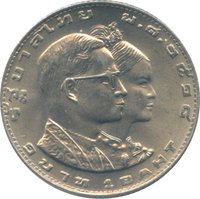

Commemoration: 25th Anniversary of the World Health Organization

Thailand

Context

Year: 1973

Thai Year: 2516

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Demonetized: Yes

Total mintage: 1,000,000

Material

Diameter: 27 mm

Weight: 7.5 g

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

Y: #Click to copy to clipboard99

Numista: #12262

Value

Exchange value: 1 THB = $0.03

Obverse

Reverse

Description:

WHO

Inscription:

25TH ANNIVERSARY

รัฐบาลไทย

๑ บาท

W.H.O.

๒๕๑๖ 1973

รัฐบาลไทย

๑ บาท

W.H.O.

๒๕๑๖ 1973

Translation:

25TH ANNIVERSARY

Thai Government

One Baht

W.H.O.

2516 1973

Thai Government

One Baht

W.H.O.

2516 1973

Language: English and Thai

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1973 | — | 1,000,000 |

Historical background

In 1973, Thailand's currency situation was characterized by stability under the long-standing fixed exchange rate regime pegged to the U.S. dollar at approximately 20.8 baht per dollar, a parity maintained since 1963. This stability was a cornerstone of the economic policy orchestrated by Field Marshal Thanom Kittikachorn's military government, which prioritized a predictable environment for foreign investment and trade. The peg was managed by the Bank of Thailand and supported by substantial foreign exchange reserves, bolstered by growing revenues from agricultural exports (notably rice and tapioca) and the increasing presence of U.S. military spending related to the Vietnam War.

However, this external stability masked significant internal economic pressures and social inequities that contributed to the political upheaval of October 1973. Rapid economic growth was unevenly distributed, leading to high inflation, rising cost of living, and growing discontent among students, urban workers, and farmers. While the baht's fixed value facilitated imports and elite business interests, it did little to alleviate the financial strain on the populace, fueling grievances against the authoritarian regime.

The political explosion in October 1973, which culminated in a violent military crackdown and the fall of the Thanom government, did not immediately disrupt the currency peg, which remained formally intact. Nevertheless, the events underscored the deep socio-economic tensions underlying the seemingly stable financial system. The new civilian government that followed inherited the challenge of addressing inflationary pressures and structural economic issues within the framework of a fixed exchange rate, setting the stage for future economic policy debates in the years to come.

However, this external stability masked significant internal economic pressures and social inequities that contributed to the political upheaval of October 1973. Rapid economic growth was unevenly distributed, leading to high inflation, rising cost of living, and growing discontent among students, urban workers, and farmers. While the baht's fixed value facilitated imports and elite business interests, it did little to alleviate the financial strain on the populace, fueling grievances against the authoritarian regime.

The political explosion in October 1973, which culminated in a violent military crackdown and the fall of the Thanom government, did not immediately disrupt the currency peg, which remained formally intact. Nevertheless, the events underscored the deep socio-economic tensions underlying the seemingly stable financial system. The new civilian government that followed inherited the challenge of addressing inflationary pressures and structural economic issues within the framework of a fixed exchange rate, setting the stage for future economic policy debates in the years to come.

🌱 Fairly Common