1 Piastra – Papal States

Vatican City

Context

Year: 1677

Country: Vatican City

Issuer: Papal States

Ruler: Innocent XI

Currency:

(1534—1835)

Demonetized: Yes

Material

References

KM: #Click to copy to clipboard398

Numista: #128265

Value

Bullion value: $84.74

Obverse

Reverse

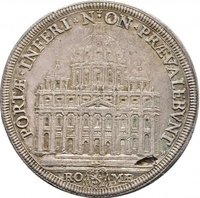

Description:

St. Peter's Basilica facade with arms below.

Inscription:

PORTÆ٠INFERI٠NON٠PRÆVALEBVNT

ROMÆ

ROMÆ

Script: Latin

Edge

Mints

| Name | Mark |

|---|---|

| Rome | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1677 | — | — |

Historical background

In 1677, the Papal States operated under a complex and strained monetary system, typical of many Italian states in the early modern period. The primary unit of account was the scudo, a silver coin, but the actual circulating currency was a bewildering array of physical coins from various Italian and foreign mints, including giuli, baiochi, and quattrini. Crucially, the value of these coins was not fixed by their metal content alone but was often set by papal decree (corso forzoso), creating a disconnect between intrinsic and official value. This practice, combined with chronic budget deficits from lavish court expenditure and military costs, placed the papal finances under constant pressure.

The situation was further complicated by the widespread practice of clipping and debasement. To raise revenue without overt taxation, the Apostolic Chamber periodically issued lighter or baser alloy coins while demanding taxes be paid in full-weight scudo. This effectively created a hidden tax, eroding public trust and leading to hoarding of older, purer coins (Gresham's Law in action). Consequently, exchange rates between different coin types fluctuated, causing confusion in trade and hardship for the common people, who dealt in low-denomination copper, while the state's debts were reckoned in silver.

Pope Innocent XI, who ascended the throne in 1676, inherited this precarious system. Known for his personal austerity and fiscal rigor, his early pontificate was marked by attempts to stabilize the currency and reduce the crushing public debt. While comprehensive reform was slow, the year 1677 fell within a period of acknowledged crisis and nascent efforts to impose order, though the fundamental structural issues of papal finance and the mixed monetary landscape would persist for centuries.

The situation was further complicated by the widespread practice of clipping and debasement. To raise revenue without overt taxation, the Apostolic Chamber periodically issued lighter or baser alloy coins while demanding taxes be paid in full-weight scudo. This effectively created a hidden tax, eroding public trust and leading to hoarding of older, purer coins (Gresham's Law in action). Consequently, exchange rates between different coin types fluctuated, causing confusion in trade and hardship for the common people, who dealt in low-denomination copper, while the state's debts were reckoned in silver.

Pope Innocent XI, who ascended the throne in 1676, inherited this precarious system. Known for his personal austerity and fiscal rigor, his early pontificate was marked by attempts to stabilize the currency and reduce the crushing public debt. While comprehensive reform was slow, the year 1677 fell within a period of acknowledged crisis and nascent efforts to impose order, though the fundamental structural issues of papal finance and the mixed monetary landscape would persist for centuries.

✨ Legendary