Obverse

Description:

Marianne bust in profile.

Inscription:

REPVBLIQVE FRANÇAISE

19 33

L.BAZOR

19 33

L.BAZOR

Translation:

FRENCH REPUBLIC

1933

L.BAZOR

1933

L.BAZOR

Script: Latin

Language: French

Engraver: Lucien Georges Bazor

Reverse

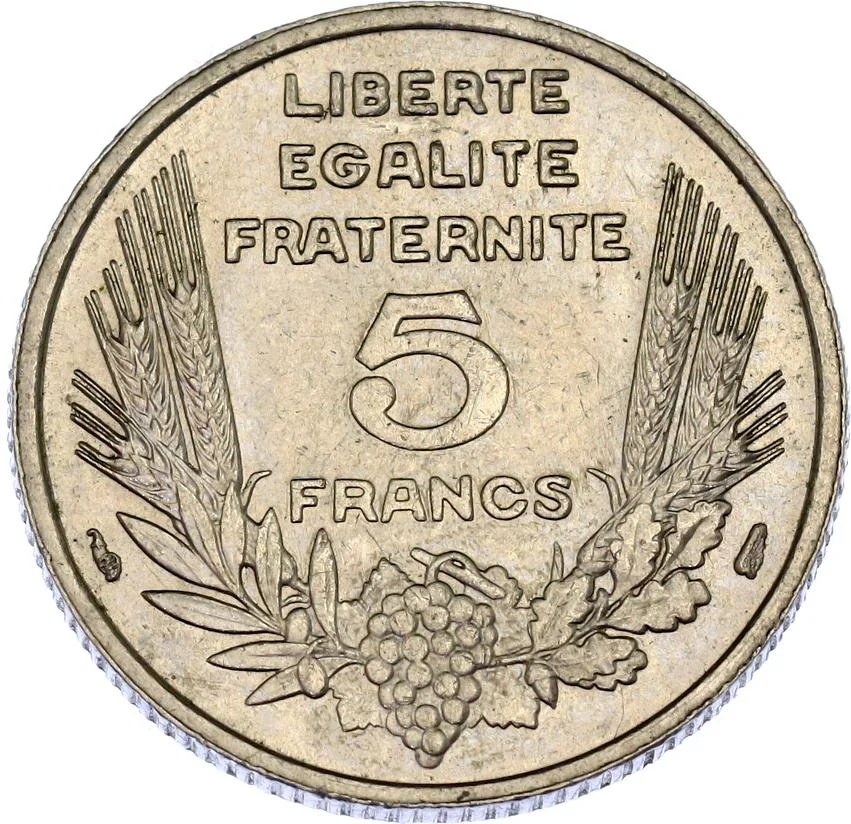

Description:

Denomination

Inscription:

LIBERTE

EGALITE

FRATERNITE

5

FRANCS

EGALITE

FRATERNITE

5

FRANCS

Translation:

LIBERTY

EQUALITY

FRATERNITY

5

FRANCS

EQUALITY

FRATERNITY

5

FRANCS

Script: Latin

Language: French

Engraver: Lucien Georges Bazor

Edge

Reeded

Categories

| Plant> Fruit |

| Symbol> Phrygian cap |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1933 | — | 160,078,050 |

Historical background

In 1933, France stood as a stark exception to the global economic turmoil of the Great Depression, initially appearing as an "island of stability." This relative strength was largely due to its adherence to the Gold Standard at the pre-war parity, a policy of franc fort (strong franc) championed by the Bank of France. While other nations, like Britain and the United States, had devalued their currencies and abandoned gold, France's conservative financial orthodoxy attracted massive gold inflows, building the world's second-largest gold reserve. This created a short-lived illusion of prosperity, with a stable currency and lower inflation than its neighbors.

However, this stability was deceptive and ultimately unsustainable. The overvalued franc made French exports prohibitively expensive on the world market, crippling key industries like textiles and agriculture. Meanwhile, cheaper foreign imports flooded the domestic market. The result was a deflationary crisis distinct from the inflationary collapses elsewhere; prices and wages fell, profits evaporated, and unemployment rose, leading to social unrest. By 1933, France was entering what economists call the "Great Depression lag," as the very policies that initially shielded it began to deepen its economic stagnation and budget deficits.

Consequently, 1933 became a pivotal year of mounting pressure on the franc. Political instability—with governments falling rapidly—prevented decisive action. Fierce debates raged between "deflationists," who advocated for brutal budget cuts to defend the gold parity at all costs, and "devaluationists," who saw currency adjustment as inevitable. While the actual devaluation of the franc would not occur until the Popular Front government of 1936, the economic contradictions of 1933 made it clear that France's rigid currency policy was a straitjacket, setting the stage for the financial and political battles of the mid-1930s.

However, this stability was deceptive and ultimately unsustainable. The overvalued franc made French exports prohibitively expensive on the world market, crippling key industries like textiles and agriculture. Meanwhile, cheaper foreign imports flooded the domestic market. The result was a deflationary crisis distinct from the inflationary collapses elsewhere; prices and wages fell, profits evaporated, and unemployment rose, leading to social unrest. By 1933, France was entering what economists call the "Great Depression lag," as the very policies that initially shielded it began to deepen its economic stagnation and budget deficits.

Consequently, 1933 became a pivotal year of mounting pressure on the franc. Political instability—with governments falling rapidly—prevented decisive action. Fierce debates raged between "deflationists," who advocated for brutal budget cuts to defend the gold parity at all costs, and "devaluationists," who saw currency adjustment as inevitable. While the actual devaluation of the franc would not occur until the Popular Front government of 1936, the economic contradictions of 1933 made it clear that France's rigid currency policy was a straitjacket, setting the stage for the financial and political battles of the mid-1930s.

🌱 Very Common