2 Bolivars – Venezuela

Venezuela

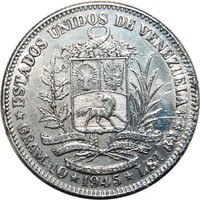

Obverse

Reverse

Edge

Reeded

Categories

| Animal> Horse |

| Person> Military leader |

| Person> Politician |

| Symbols> Coat of Arms |

| Symbol> Cornucopia |

Mints

| Name | Mark |

|---|---|

| United States Mint of Philadelphia | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1947 | — | 3,000,000 |

Historical background

In 1947, Venezuela's currency situation was one of notable stability and strength, particularly within the Latin American context. The national currency, the bolívar, was firmly pegged to the US dollar at a fixed rate of 3.09 bolívares to the dollar, a parity established in 1941. This stability was underpinned by a rapidly growing petroleum-export economy, which provided the government with substantial foreign exchange reserves. As oil production surged in the post-World War II period, Venezuela became a leading global exporter, flooding state coffers with dollars and ensuring full convertibility for the bolívar.

This monetary stability was managed by the Banco Central de Venezuela (BCV), established just seven years prior in 1940. The BCV's conservative policies, including maintaining high international reserves, were instrumental in defending the fixed exchange rate. The era was characterized by low inflation and a strong, credible currency that facilitated both international trade and domestic economic planning. The bolívar was so robust that it was colloquially referred to as "the dollar of Latin America," attracting foreign investment and contributing to a period of significant national infrastructure and industrial development known as the "Venezuelan Miracle."

However, this picture of strength was fundamentally dependent on a single commodity. The entire monetary and fiscal structure rested on the continued high revenue from oil exports, creating a vulnerable, rentier economy. While 1947 itself saw no crisis—occurring during a democratic interlude after the death of Juan Vicente Gómez and before the military coup of 1948—it represented the peak of this oil-fueled monetary stability. The period highlighted a structural weakness: the state's finances and the currency's value were not tied to diversified productive capacity but to volatile global oil markets, a dependency that would pose severe challenges in the decades to follow.

This monetary stability was managed by the Banco Central de Venezuela (BCV), established just seven years prior in 1940. The BCV's conservative policies, including maintaining high international reserves, were instrumental in defending the fixed exchange rate. The era was characterized by low inflation and a strong, credible currency that facilitated both international trade and domestic economic planning. The bolívar was so robust that it was colloquially referred to as "the dollar of Latin America," attracting foreign investment and contributing to a period of significant national infrastructure and industrial development known as the "Venezuelan Miracle."

However, this picture of strength was fundamentally dependent on a single commodity. The entire monetary and fiscal structure rested on the continued high revenue from oil exports, creating a vulnerable, rentier economy. While 1947 itself saw no crisis—occurring during a democratic interlude after the death of Juan Vicente Gómez and before the military coup of 1948—it represented the peak of this oil-fueled monetary stability. The period highlighted a structural weakness: the state's finances and the currency's value were not tied to diversified productive capacity but to volatile global oil markets, a dependency that would pose severe challenges in the decades to follow.

🌱 Common