500 yen – Japan

Add to wishlist

Circulating commemorative coins

Commemoration: Opening of the Seto Bridge

Japan

Context

Year: 1988

Japanese - Shōwa era Year:: 63

Issuer: Japan

Ruler: Shōwa

Currency:

(since 1871)

Total mintage: 20,000,000

Material

References

Y: #

Numista: #10961

Value

Exchange value: 500 JPY

Inflation-adjusted value: 643.96 JPY

Obverse

Description:

Seto Bridge: authority above, value below.

Inscription:

日 本 国

五 百 円

五 百 円

Translation:

Japan

Five Hundred Yen

Five Hundred Yen

Language: Japanese

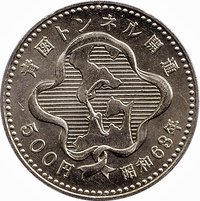

Reverse

Description:

Honshu in a ribbon, legends encircling.

Inscription:

瀬 戸 大 橋 開 通

500円 昭和63年

500円 昭和63年

Translation:

Seto Ohashi Opening

500 Yen, Showa 63

500 Yen, Showa 63

Language: Japanese

Edge

Reeded with text

Legend:

SETO BRIDGE '88 ◆ 88, ƎפpIɹq O┴ƎS ◆

Translation:

SETO BRIDGE '88 ◆ 88, BRIDGE SETO ◆

Language: English

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | 20,000,000 |

Historical background

In 1988, Japan's currency situation was dominated by the dramatic appreciation of the yen following the Plaza Accord of 1985. The agreement, designed to correct global trade imbalances, saw major economies intervene to weaken the US dollar. This led to the yen's value soaring from around 240 yen to the dollar in 1985 to approximately 128 yen by the end of 1988. This sharp endaka (high yen) presented a dual challenge: it severely squeezed the profitability of Japan's export-driven industries like automobiles and electronics, while simultaneously increasing the purchasing power of Japanese corporations and individuals abroad.

Domestically, the strong yen contributed to the speculative excesses of the "bubble economy." To counteract the deflationary pressure of the high yen and a recession in 1986, the Bank of Japan implemented an extended period of extremely low interest rates. This cheap money, combined with corporate profits from earlier exports, flooded into domestic asset markets, inflating massive bubbles in real estate and stock prices. The currency's strength also fueled a wave of overseas investment and acquisitions, as Japanese entities found foreign assets and companies suddenly more affordable, leading to high-profile purchases of iconic foreign properties.

By 1988, policymakers faced a complex dilemma. The yen's strength was a testament to Japan's economic might but threatened its industrial core. The government and the Bank of Japan were attempting a delicate balancing act: managing the yen's volatility through occasional intervention while cautiously tightening monetary policy to address the domestic asset bubble, without triggering a further yen appreciation that would harm exports. The currency situation was thus a central and precarious element of the late-1980s bubble, embedding vulnerabilities that would culminate in its collapse in the early 1990s.

Domestically, the strong yen contributed to the speculative excesses of the "bubble economy." To counteract the deflationary pressure of the high yen and a recession in 1986, the Bank of Japan implemented an extended period of extremely low interest rates. This cheap money, combined with corporate profits from earlier exports, flooded into domestic asset markets, inflating massive bubbles in real estate and stock prices. The currency's strength also fueled a wave of overseas investment and acquisitions, as Japanese entities found foreign assets and companies suddenly more affordable, leading to high-profile purchases of iconic foreign properties.

By 1988, policymakers faced a complex dilemma. The yen's strength was a testament to Japan's economic might but threatened its industrial core. The government and the Bank of Japan were attempting a delicate balancing act: managing the yen's volatility through occasional intervention while cautiously tightening monetary policy to address the domestic asset bubble, without triggering a further yen appreciation that would harm exports. The currency situation was thus a central and precarious element of the late-1980s bubble, embedding vulnerabilities that would culminate in its collapse in the early 1990s.

🌟 Uncommon