1 Rupee – India - British

India

Context

Year: 1840

Country: India

Issuer: India - British

Issuing organization: East India Company

Ruler: Victoria

Currency:

(1770—1947)

Demonetized: Yes

Material

References

KM: #Click to copy to clipboard457

Numista: #9718

Value

Bullion value: $30.34

Obverse

Description:

Queen Victoria, left-facing portrait.

Inscription:

VICTORIA QUEEN

Script: Latin

Engraver: William Wyon

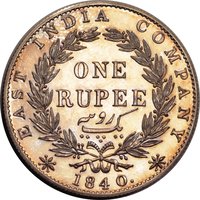

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Chennai / Madras | — |

| Kolkata / Calcutta / Murshidabad | — |

| Mumbai / Bombay | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1840 | — | — | ||

| 1840 | — | — | Proof |

Historical background

By 1840, the currency situation in British India was a complex and often chaotic system, caught between India's ancient monetary traditions and the demands of a colonial economy. The dominant official currency was the silver rupee, primarily the Company's "Sicca Rupee" minted in Calcutta, but its value and purity varied significantly against other regional rupees (like the Bombay and Madras rupees). Alongside these, gold mohurs circulated at a fluctuating rate, and a vast sea of older, often debased Mughal and local princely coins remained in use, creating a nightmare for commerce and tax collection. The British East India Company, governing large territories, struggled to impose a uniform standard.

The core economic problem was a chronic shortage of small-denomination coins for everyday transactions, leading to the continued use of cut and broken pieces of silver rupees (dammas) and a plethora of local cowrie shells, copper pice, and other informal tokens. Furthermore, the British policy of "free trade" in bullion meant gold and silver could be freely imported and exported. This exposed India's currency to global fluctuations, notably the drain of silver to finance the Opium Trade and to meet China's demand for silver, which periodically caused scarcity and economic strain.

In response, the Company was in a slow process of reform. The Coinage Act of 1835 had established a unified system based on a single silver rupee standard (180 grains, 11/12 fine) bearing the image of William IV, aiming to replace the older varieties. By 1840, these new uniform rupees were being minted and circulated, but the transition was far from complete. The period thus represents a pivotal moment—the waning of the old fragmented system and the hesitant, uneven imposition of a colonial monetary standard designed to streamline administration and integrate India more firmly into the British imperial economy.

The core economic problem was a chronic shortage of small-denomination coins for everyday transactions, leading to the continued use of cut and broken pieces of silver rupees (dammas) and a plethora of local cowrie shells, copper pice, and other informal tokens. Furthermore, the British policy of "free trade" in bullion meant gold and silver could be freely imported and exported. This exposed India's currency to global fluctuations, notably the drain of silver to finance the Opium Trade and to meet China's demand for silver, which periodically caused scarcity and economic strain.

In response, the Company was in a slow process of reform. The Coinage Act of 1835 had established a unified system based on a single silver rupee standard (180 grains, 11/12 fine) bearing the image of William IV, aiming to replace the older varieties. By 1840, these new uniform rupees were being minted and circulated, but the transition was far from complete. The period thus represents a pivotal moment—the waning of the old fragmented system and the hesitant, uneven imposition of a colonial monetary standard designed to streamline administration and integrate India more firmly into the British imperial economy.

🌱 Common